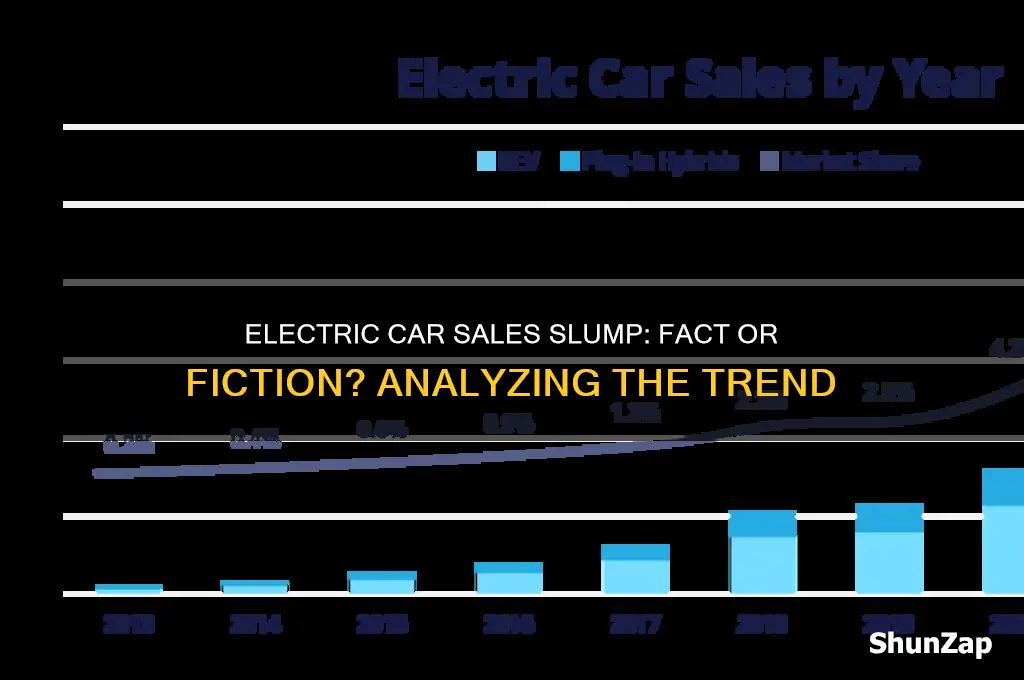

The question of whether sales of electric cars are declining has sparked considerable debate in the automotive industry. While electric vehicles (EVs) have experienced rapid growth over the past decade, recent data suggests a potential slowdown in certain markets. Factors such as rising interest rates, supply chain disruptions, and increased competition from hybrid vehicles have contributed to this trend. Additionally, concerns about charging infrastructure and range anxiety persist, influencing consumer behavior. However, it’s important to note that global EV sales continue to rise overall, driven by strong demand in regions like China and Europe. The apparent decline in some markets may reflect temporary challenges rather than a long-term shift, as governments and automakers remain committed to electrification goals.

| Characteristics | Values |

|---|---|

| Global Trend (2023) | Electric vehicle (EV) sales continued to grow globally in 2023, with an estimated 14% increase compared to 2022. |

| Regional Variations | Sales growth varies by region. Europe and China saw strong growth, while the U.S. market experienced slower growth due to economic factors and charging infrastructure concerns. |

| Market Share | EVs accounted for approximately 18% of global car sales in 2023, up from 14% in 2022. |

| Declining Sales in Specific Markets | Some markets, such as Norway (a leader in EV adoption), saw a slight decline in EV sales growth rate in 2023 due to reduced incentives and increased competition from hybrid vehicles. |

| Factors Influencing Sales | Government incentives, charging infrastructure development, battery technology advancements, and consumer preferences play a significant role in EV sales trends. |

| Future Outlook | Analysts predict continued global EV sales growth, with projections reaching over 30% market share by 2030. |

Explore related products

What You'll Learn

- Market Trends: Recent data shows fluctuations in electric vehicle (EV) sales across regions

- Economic Factors: Rising costs and inflation impact consumer willingness to buy EVs

- Supply Chain Issues: Chip shortages and battery material scarcity affect production and sales

- Consumer Sentiment: Range anxiety and charging infrastructure concerns still deter potential buyers

- Competitive Landscape: Increased competition from traditional automakers and hybrid models challenges EV dominance

![]()

Market Trends: Recent data shows fluctuations in electric vehicle (EV) sales across regions

Recent data reveals a nuanced picture of electric vehicle (EV) sales, with fluctuations across regions that defy a simple narrative of decline or growth. In North America, for instance, EV sales surged by 50% in 2023, driven by federal tax incentives and expanding charging infrastructure. However, this growth is unevenly distributed, with states like California leading the charge while others lag due to limited policy support and consumer skepticism. This regional disparity underscores the importance of localized strategies in fostering EV adoption.

Contrastingly, Europe experienced a 10% dip in EV sales in the same period, marking the first decline in a decade. Analysts attribute this to rising energy costs, supply chain disruptions, and reduced subsidies in key markets like Germany and the UK. Yet, Norway remains an outlier, with EVs accounting for 80% of new car sales, buoyed by aggressive government incentives and a mature charging network. This highlights how policy consistency and infrastructure investment can insulate markets from broader economic headwinds.

In Asia, the EV landscape is equally dynamic. China, the world’s largest EV market, saw a 20% increase in sales, propelled by stringent emissions regulations and domestic manufacturing dominance. Meanwhile, India’s EV market grew by 150%, albeit from a low base, as government initiatives like the FAME II scheme and falling battery costs begin to take effect. However, Japan’s EV sales remain stagnant, with hybrid vehicles still dominating consumer preference, reflecting cultural and infrastructural barriers to full electrification.

These regional fluctuations suggest that EV adoption is not a monolithic trend but a mosaic shaped by economic, policy, and cultural factors. For instance, regions with robust incentives, reliable charging networks, and consumer awareness tend to outperform. Conversely, markets facing economic uncertainty or policy volatility often see slower growth. Practical takeaways include the need for tailored regional strategies, such as increasing public charging stations in rural areas or offering targeted incentives for low-income buyers.

Ultimately, while global EV sales continue to rise, the pace and pattern of growth vary widely. Policymakers, manufacturers, and consumers must recognize these regional nuances to navigate the transition effectively. By addressing specific barriers—whether infrastructure gaps, affordability concerns, or consumer education—stakeholders can ensure that the EV revolution remains on track, even in the face of localized fluctuations.

Electric Vehicle Companies: A Monotonous, Uninspiring Future?

You may want to see also

Explore related products

![]()

Economic Factors: Rising costs and inflation impact consumer willingness to buy EVs

The surge in electric vehicle (EV) prices over the past year has been staggering, with some models seeing increases of up to 20%. This isn't just a minor adjustment—it's a significant shift that directly impacts consumer behavior. For instance, the average price of a new EV in the U.S. has risen to over $60,000, compared to $48,000 for traditional gasoline vehicles. Such a disparity makes EVs less accessible, especially for middle-income households. When coupled with rising interest rates, which have increased monthly loan payments by as much as 30%, the financial burden becomes even more daunting. This economic pressure is forcing many potential buyers to reconsider their decision to go electric, opting instead for more affordable alternatives.

Consider the ripple effect of inflation on raw materials critical to EV production, such as lithium and cobalt. Prices for these commodities have skyrocketed, with lithium carbonate prices increasing by 400% in the past two years. Manufacturers are passing these costs onto consumers, further inflating the price tag of EVs. For families already grappling with higher grocery bills and energy costs, an EV purchase becomes a luxury rather than a necessity. A recent survey by J.D. Power revealed that 45% of consumers cited affordability as the primary barrier to EV adoption, overshadowing concerns like charging infrastructure and range anxiety.

To illustrate, let’s compare two scenarios. A 35-year-old professional earning $70,000 annually might have budgeted for a $45,000 EV two years ago. Today, that same vehicle costs $54,000, a 20% increase. With inflation eroding their purchasing power and monthly expenses rising, this buyer is now more likely to delay the purchase or opt for a hybrid or gasoline vehicle. Multiply this scenario across millions of consumers, and the decline in EV sales becomes more understandable. It’s not just about the sticker price—it’s the cumulative effect of economic pressures on household budgets.

Here’s a practical tip for consumers navigating this landscape: If you’re considering an EV, factor in not just the upfront cost but also long-term savings on fuel and maintenance. Use online calculators to compare total ownership costs between EVs and traditional vehicles. Additionally, explore federal and state incentives, which can offset up to $7,500 of the purchase price. For example, leasing an EV can be a more affordable entry point, with monthly payments often comparable to those of gasoline vehicles. However, be cautious of mileage limits and residual value clauses in lease agreements.

In conclusion, the economic headwinds of rising costs and inflation are reshaping the EV market. While EVs remain a critical component of the transition to sustainable transportation, their accessibility is being compromised by financial barriers. Policymakers, manufacturers, and consumers must work together to address these challenges, whether through price stabilization, expanded incentives, or innovative financing options. Without such measures, the decline in EV sales could persist, slowing progress toward a greener future.

Mastering the Smooth Shift: A Guide to Electric Car Gear Changes

You may want to see also

Explore related products

![]()

Supply Chain Issues: Chip shortages and battery material scarcity affect production and sales

The global semiconductor chip shortage, a lingering aftermath of the COVID-19 pandemic, has become a significant bottleneck for the electric vehicle (EV) industry. These tiny components are the brains behind modern vehicles, controlling everything from infotainment systems to advanced driver-assistance features. With the average EV requiring up to 2,000 chips, the shortage has led to production delays and reduced output for major automakers. For instance, Tesla, despite its robust sales figures, has faced challenges in meeting demand due to chip-related constraints. This issue is not isolated; it’s a widespread problem affecting both established manufacturers and startups, creating a ripple effect that slows down the entire EV market.

Compounding the chip shortage is the growing scarcity of critical battery materials, such as lithium, cobalt, and nickel. The demand for these resources has skyrocketed as EV production scales up, but supply chains struggle to keep pace. Lithium, for example, has seen price increases of over 400% in recent years, driven by limited mining capacity and geopolitical tensions. Cobalt, primarily sourced from the Democratic Republic of Congo, faces ethical and logistical challenges, while nickel supply is constrained by shifting production priorities in Indonesia. These material shortages not only drive up battery costs but also limit the number of EVs that can be produced, creating a supply-demand imbalance that stifles sales growth.

To mitigate these challenges, automakers are adopting both short-term fixes and long-term strategies. In the immediate term, companies are redesigning vehicles to use fewer chips or alternative components, though this often comes at the expense of features or performance. Some manufacturers are also securing direct supply agreements with chipmakers and material suppliers to ensure priority access. Long-term solutions include investing in chip manufacturing capabilities, diversifying material sourcing, and exploring new battery chemistries that reduce reliance on scarce resources. For instance, Tesla’s shift toward lithium iron phosphate (LFP) batteries, which eliminate the need for nickel and cobalt, is a strategic move to address material scarcity.

Despite these efforts, the supply chain issues have tangible consequences for consumers. Longer wait times for new EVs, coupled with rising prices due to material costs, have dampened some buyer enthusiasm. In regions where government incentives are insufficient to offset these increases, sales growth has slowed. For example, in Europe, EV sales growth dropped from 66% in 2021 to just 10% in 2023, partly due to supply chain-related price hikes. This highlights the delicate balance between consumer demand and production capabilities, underscoring the need for systemic solutions to sustain the EV market’s momentum.

In conclusion, while the decline in EV sales cannot be solely attributed to supply chain issues, chip shortages and battery material scarcity are undeniably significant factors. These challenges serve as a reminder of the interconnectedness of the global economy and the fragility of emerging industries. Addressing them requires collaboration across sectors, from mining and manufacturing to policy-making, to ensure that the transition to electric mobility remains on track. For consumers, staying informed about these dynamics can help manage expectations and highlight the broader implications of their purchasing decisions.

Electric Vehicles: Are They Safe?

You may want to see also

Explore related products

![200W Car Power Inverter, PiSFAU DC 12V to 110V AC Car Plug Adapter Outlet with [20W USB-C] /USB-Fast Charger(18W) / 4.8A Dual USB/car Charger for Laptop](https://m.media-amazon.com/images/I/61IRXv7G09L._AC_UL320_.jpg)

![]()

Consumer Sentiment: Range anxiety and charging infrastructure concerns still deter potential buyers

Despite the growing buzz around electric vehicles (EVs), a significant portion of potential buyers remain on the fence, and their hesitation isn’t about the cars themselves—it’s about the lifestyle shift they demand. Range anxiety, the fear of running out of battery before reaching a charging station, tops the list of concerns. For instance, a 2023 J.D. Power study revealed that 59% of consumers cite range limitations as a primary reason for avoiding EVs. This anxiety isn’t unfounded; while modern EVs boast ranges of 250–400 miles per charge, real-world conditions like cold weather, high speeds, and heavy loads can slash that figure by 20–30%. For someone accustomed to refueling in minutes and driving 500 miles on a single tank, this uncertainty feels like a step backward.

Compounding range anxiety is the patchy and often unreliable charging infrastructure. Unlike gas stations, which are ubiquitous and universally compatible, EV charging stations vary widely in availability, speed, and payment methods. A 2022 McKinsey report highlighted that the U.S. would need at least 1.2 million public chargers by 2030 to support widespread EV adoption, yet as of 2023, fewer than 150,000 exist. Even when chargers are available, they’re often occupied, out of order, or incompatible with certain vehicle models. For example, Tesla’s proprietary Supercharger network, while extensive, is exclusive to Tesla owners, leaving drivers of other brands scrambling for alternatives. This fragmentation creates a chicken-and-egg dilemma: consumers won’t buy EVs until charging is convenient, but investment in charging infrastructure lags without higher EV adoption rates.

To address these concerns, practical steps can be taken. First, automakers should focus on educating consumers about real-world range expectations and the benefits of home charging, which accounts for 80% of EV charging sessions. Installing a Level 2 home charger, costing $500–$1,200 after tax credits, can alleviate daily range anxiety. Second, policymakers and private companies must collaborate to standardize charging networks, ensuring seamless payment and compatibility across brands. For instance, the Biden administration’s $7.5 billion investment in EV infrastructure is a step in the right direction, but execution and maintenance will be key. Finally, employers and retailers can play a role by installing workplace and destination chargers, turning idle parking time into charging opportunities.

The takeaway is clear: while EVs offer environmental and economic advantages, their success hinges on addressing consumer fears head-on. Range anxiety and charging concerns aren’t insurmountable, but they require a coordinated effort from automakers, governments, and businesses. Until then, many potential buyers will remain in wait-and-see mode, leaving EV sales growth dependent on early adopters rather than the mass market.

Save Energy, Cut Costs: Why Unplug Appliances When Not in Use

You may want to see also

Explore related products

![]()

Competitive Landscape: Increased competition from traditional automakers and hybrid models challenges EV dominance

The electric vehicle (EV) market, once a niche dominated by pioneers like Tesla, is now a battleground where traditional automakers and hybrid models are gaining ground. This shift is not merely a trend but a strategic response to consumer demands and regulatory pressures. For instance, Toyota’s hybrid lineup, including the Prius and RAV4 Hybrid, has seen a 15% increase in sales year-over-year, while Ford’s F-150 Lightning electric truck is directly competing with Tesla’s Cybertruck. These examples illustrate how established brands are leveraging their manufacturing scale, dealership networks, and brand loyalty to challenge EV dominance.

Analyzing the competitive landscape reveals a critical insight: traditional automakers are no longer playing catch-up. Companies like Volkswagen, General Motors, and Hyundai are investing billions in EV technology, with Volkswagen’s ID.4 and Hyundai’s Ioniq 5 emerging as strong contenders. Meanwhile, hybrid models offer a middle ground for consumers hesitant to fully embrace EVs, providing improved fuel efficiency without the range anxiety associated with battery-only vehicles. This dual-pronged approach—expanding EV portfolios while enhancing hybrid offerings—is diluting the market share of pure EV brands.

To navigate this evolving landscape, EV manufacturers must differentiate themselves beyond range and charging speed. For example, Tesla’s Supercharger network remains a significant advantage, but competitors are rapidly building their own infrastructure. Practical tips for EV brands include focusing on software integration, such as advanced driver-assistance systems (ADAS) and over-the-air updates, which can create a unique user experience. Additionally, targeting specific demographics—like urban commuters with compact EVs or families with larger, feature-rich models—can help carve out niche markets.

A cautionary note for EV manufacturers is the risk of over-saturation. With dozens of new models entering the market annually, differentiation becomes increasingly difficult. Hybrid models, in particular, pose a threat by appealing to price-sensitive consumers. For instance, the Toyota Corolla Hybrid starts at $23,000, significantly undercutting entry-level EVs like the Chevrolet Bolt, which begins at $26,500. EV brands must balance innovation with affordability to remain competitive, especially as government incentives for EVs begin to phase out in some regions.

In conclusion, the competitive landscape for EVs is no longer defined by a single player’s dominance. Traditional automakers and hybrid models are reshaping the market, forcing EV brands to innovate beyond their core strengths. By focusing on software, targeting specific demographics, and addressing price sensitivity, EV manufacturers can maintain their relevance. However, failure to adapt to this new reality could lead to a decline in sales, as consumers are now spoiled for choice in an increasingly crowded field.

California's Role in Electric Vehicle Market Creation

You may want to see also

Frequently asked questions

No, global sales of electric cars are not declining. In fact, they continue to grow, with 2023 seeing a significant increase in sales compared to previous years, driven by advancements in technology, government incentives, and rising environmental awareness.

While growth rates may vary, electric car sales in the U.S. are not declining overall. However, some quarters may show slower growth due to factors like economic conditions, supply chain issues, or shifts in consumer preferences.

No, Europe remains a strong market for electric vehicles, with sales continuing to rise. Countries like Norway, Germany, and the UK are leading the way, supported by stringent emissions regulations and robust charging infrastructure.

China, the world’s largest EV market, continues to see strong growth in electric car sales. Government policies, local manufacturing, and consumer demand are driving this trend, with no signs of decline.