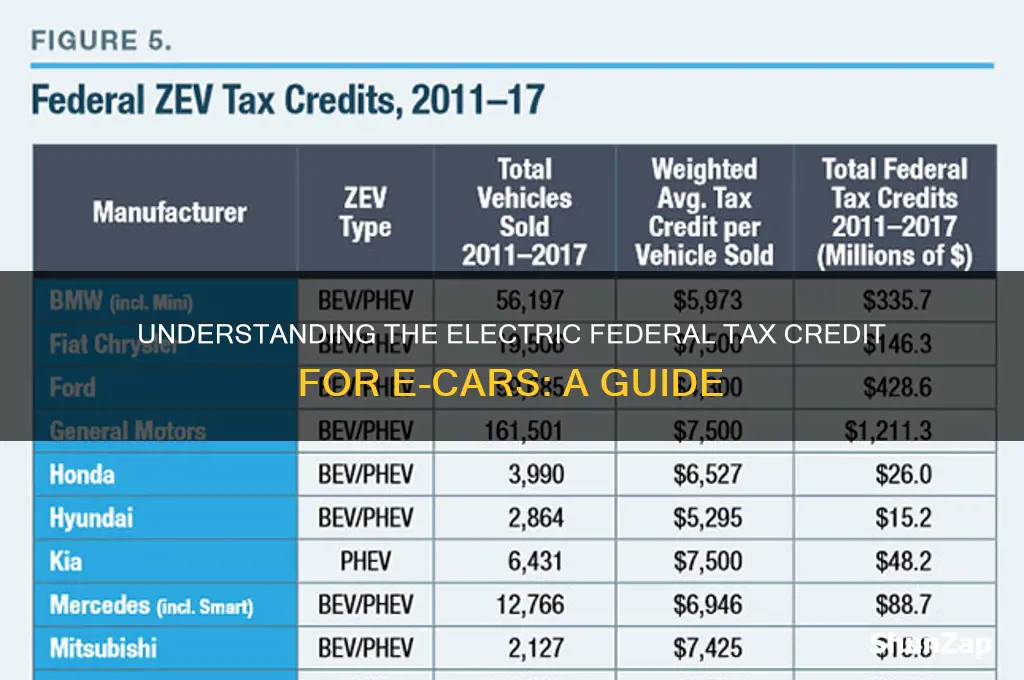

The Electric Federal Tax Credit for electric vehicles (EVs) is a financial incentive designed to encourage the adoption of eco-friendly transportation by reducing the cost of purchasing eligible electric cars. Established under the Internal Revenue Code Section 30D, this credit allows buyers to claim up to $7,500 on their federal taxes, depending on the vehicle’s battery capacity and the manufacturer’s cumulative sales. To qualify, the EV must meet specific requirements, such as being new, primarily for personal use, and manufactured by a company that hasn’t surpassed the 200,000-unit sales cap. The credit phases out once a manufacturer hits this threshold, making it essential for buyers to verify eligibility before purchase. Additionally, the credit is non-refundable, meaning it can only reduce tax liability to zero but won’t result in a refund if the credit exceeds the amount owed. Understanding these details is crucial for maximizing the benefits of this incentive while transitioning to sustainable transportation.

| Characteristics | Values |

|---|---|

| Credit Name | Qualified Plug-in Electric Drive Motor Vehicle Tax Credit (IRC 30D) |

| Eligible Vehicles | New plug-in electric vehicles (PEVs), including battery-electric (BEV) and plug-in hybrid (PHEV) vehicles. |

| Maximum Credit Amount | Up to $7,500 per vehicle (split into two components: $4,000 for battery capacity and up to $3,500 for additional battery and vehicle features). |

| Battery Capacity Requirement | Vehicles must have a battery capacity of at least 7 kilowatt-hours (kWh) to qualify for the full credit. |

| Income Limits (2023) | No income limits for new vehicles. For used vehicles, income limits apply: $150,000 for single filers, $300,000 for joint filers. |

| Manufacturer Cap | Once a manufacturer sells 200,000 qualifying vehicles, a phase-out period begins, and the credit is gradually reduced. |

| Vehicle Price Cap (New Vehicles) | SUVs, pickups, and vans: MSRP ≤ $80,000. Other vehicles: MSRP ≤ $55,000. |

| Used Vehicle Credit (IRC 25E) | Up to $4,000 or 30% of the vehicle’s sale price, whichever is less. Vehicle must be at least 2 years old, and buyer’s income must meet limits. |

| North American Assembly Requirement | Vehicles must be assembled in North America to qualify for the credit. |

| Battery Component Requirements | Starting 2024, a percentage of critical minerals and battery components must be sourced from the U.S. or free trade partners. |

| Leased Vehicles | Credit goes to the leasing company, not the lessee. |

| Effective Date for New Rules | Most changes (e.g., North American assembly, battery requirements) took effect in 2023. |

| IRS Guidance | IRS provides a list of eligible vehicles and updates requirements periodically. |

| Tax Credit vs. Rebate | Non-refundable credit (reduces tax liability but does not provide a refund if liability is zero). |

| Transferability (Future) | Starting 2024, credits may be transferable to dealers for upfront discounts (details pending). |

Explore related products

What You'll Learn

- Eligibility Requirements: Income limits, car price caps, and battery capacity rules for tax credit qualification

- Credit Amounts: Maximum credit values based on battery size and vehicle type

- Manufacturer Caps: Phase-out limits after 200,000 eligible vehicles sold per automaker

- Used EV Credits: Up to $4,000 for pre-owned electric vehicles meeting criteria

- Claiming Process: IRS Form 8936 filing details for tax credit redemption

![]()

Eligibility Requirements: Income limits, car price caps, and battery capacity rules for tax credit qualification

The electric vehicle (EV) federal tax credit is a significant incentive for consumers looking to purchase electric cars, but it comes with specific eligibility requirements. One of the key criteria is income limits. As of the latest updates, the tax credit is phased out for single taxpayers with a modified adjusted gross income (MAGI) exceeding $150,000, for married couples filing jointly with a MAGI above $300,000, and for heads of households with a MAGI over $225,000. Once a taxpayer’s income surpasses these thresholds, the credit is gradually reduced until it is no longer available. This ensures that the incentive primarily benefits middle- and lower-income households, aligning with the goal of making EVs more accessible to a broader population.

Another critical eligibility requirement is the car price cap. Under current regulations, eligible electric vehicles must have a manufacturer’s suggested retail price (MSRP) below $55,000 for cars and $80,000 for SUVs, trucks, and vans. This rule prevents the tax credit from subsidizing luxury vehicles, focusing instead on more affordable options. It’s important for buyers to verify the MSRP of the specific EV model they are considering, as exceeding these price caps disqualifies the vehicle from the tax credit, regardless of other eligibility factors.

Battery capacity rules also play a pivotal role in determining tax credit qualification. To be eligible, an electric vehicle must be equipped with a battery pack with a minimum capacity of 7 kilowatt-hours (kWh). Additionally, the credit amount is tiered based on battery size, with a maximum credit of $7,500 available for vehicles with battery capacities of 16 kWh or greater. Vehicles with smaller battery packs may qualify for a partial credit, calculated at $417 per kWh, up to a maximum of $7,500. This requirement ensures that the tax credit supports vehicles with substantial electric range, promoting the adoption of more practical and environmentally friendly EVs.

It’s essential for potential buyers to note that these eligibility requirements are subject to change as federal policies evolve. For instance, the Inflation Reduction Act of 2022 introduced new rules, including the income limits and price caps mentioned earlier, which took effect in 2023. Buyers should consult the latest IRS guidelines or a tax professional to ensure their purchase meets all current criteria. Additionally, the tax credit is non-refundable, meaning it can only reduce the taxpayer’s liability to zero but does not provide a refund beyond that. Understanding these eligibility requirements is crucial for maximizing the benefits of the electric vehicle federal tax credit.

Electric Tool Safety: Identifying the Most Common Hazard to Avoid

You may want to see also

Explore related products

![]()

Credit Amounts: Maximum credit values based on battery size and vehicle type

The electric vehicle (EV) federal tax credit, officially known as the Qualified Plug-in Electric Drive Motor Vehicle Credit (IRC 30D), offers financial incentives to buyers of new electric and plug-in hybrid vehicles. The credit amounts are not one-size-fits-all; they vary based on critical factors such as battery size and vehicle type. For eligible vehicles, the credit is determined by the capacity of the battery pack, measured in kilowatt-hours (kWh). The larger the battery, the higher the potential credit, up to a maximum threshold. As of recent updates, the credit structure is designed to encourage the adoption of EVs with more substantial battery capacities, which generally offer greater electric range and environmental benefits.

For battery electric vehicles (BEVs), which run exclusively on electricity, the credit starts at a base amount and increases incrementally with battery size. Vehicles with a battery capacity of at least 7 kWh but less than 16 kWh qualify for a minimum credit, while those with 16 kWh or more can receive the full credit amount, currently capped at $7,500. This tiered approach ensures that vehicles with larger batteries, which typically have longer ranges and contribute more to reducing emissions, receive greater incentives. It’s important to note that the credit phases out once a manufacturer sells 200,000 qualifying vehicles, so availability depends on the automaker’s sales milestones.

Plug-in hybrid electric vehicles (PHEVs) also qualify for the credit, but the amount is generally lower than for BEVs. PHEVs combine an electric motor with a traditional internal combustion engine and have smaller battery packs. The credit for PHEVs is calculated based on their battery capacity, with a minimum threshold of 5 kWh. The maximum credit for PHEVs is typically lower than for BEVs, reflecting their smaller battery size and shorter electric-only range. For example, a PHEV with a 10 kWh battery might qualify for a credit of $2,500, while a BEV with a 20 kWh battery could receive the full $7,500.

The vehicle type also plays a role in determining credit eligibility. Only new, qualifying vehicles purchased for personal or business use are eligible. Leased vehicles may qualify for a separate credit claimed by the leasing company, which may pass savings on to the lessee. Additionally, the vehicle’s manufacturer suggested retail price (MSRP) must fall below a certain threshold for SUVs, trucks, and vans (up to $80,000) and cars (up to $55,000) to qualify for the credit. This ensures that the incentive targets affordable and widely accessible EV models.

Lastly, the credit is non-refundable, meaning it can reduce the taxpayer’s federal income tax liability to zero but cannot provide a refund beyond that. However, any unused portion of the credit can be carried over to future tax years until fully utilized. Understanding these credit amounts based on battery size and vehicle type is crucial for maximizing the financial benefits of purchasing an electric vehicle and contributing to a more sustainable transportation ecosystem.

Best Oil for Greenworks 18 Electric Chainsaw Maintenance Guide

You may want to see also

Explore related products

![]()

Manufacturer Caps: Phase-out limits after 200,000 eligible vehicles sold per automaker

The electric vehicle (EV) federal tax credit is a significant incentive designed to promote the adoption of electric cars in the United States. However, this credit is not unlimited, particularly when it comes to the number of vehicles an automaker can sell while still qualifying for the incentive. The Manufacturer Caps: Phase-out limits after 200,000 eligible vehicles sold per automaker is a critical component of this program. Once an automaker reaches the threshold of 200,000 eligible EVs sold, the tax credit begins to phase out for that manufacturer’s vehicles. This cap ensures that the incentive remains targeted and prevents large-scale automakers from dominating the benefits indefinitely.

The phase-out process is structured in two stages after the 200,000-vehicle threshold is crossed. In the first stage, which begins in the second quarter after the threshold is reached, the tax credit is reduced to 50% of its original value. For example, if the original credit was $7,500, it would drop to $3,750. In the second stage, which starts two quarters later, the credit is further reduced to 25% of its original value, or $1,875 in this example. After these two stages, the tax credit is completely eliminated for that automaker’s vehicles. This gradual reduction allows consumers and manufacturers to adjust to the changes without abrupt disruptions.

It’s important to note that the 200,000-vehicle cap applies to each individual automaker, not the industry as a whole. This means that while one manufacturer may be phasing out of the credit, others may still be offering the full incentive if they haven’t yet reached the threshold. This system encourages competition among automakers to produce and sell EVs early, while also ensuring that newer entrants or smaller manufacturers can still benefit from the credit later on.

The manufacturer cap has significant implications for both consumers and automakers. For consumers, it means that the availability and amount of the tax credit depend on the automaker’s sales history. Prospective EV buyers should research whether their preferred manufacturer has reached the phase-out threshold to understand the potential credit they can receive. For automakers, the cap creates a strategic challenge, as they must balance the pace of EV production and sales to maximize the benefit of the tax credit for their customers while planning for the eventual phase-out.

Legislation and updates to the EV tax credit, such as those included in the Inflation Reduction Act of 2022, have introduced changes to how the manufacturer cap is applied. For instance, some revisions aim to extend or modify the credit to further incentivize EV adoption. However, the core principle of the manufacturer cap remains intact, ensuring that the incentive remains equitable and sustainable. Understanding these limits is essential for anyone involved in the EV market, from manufacturers to consumers, as it directly impacts the financial incentives available for purchasing electric vehicles.

Electric Car Lifespan: How Long Do They Really Last?

You may want to see also

Explore related products

![]()

Used EV Credits: Up to $4,000 for pre-owned electric vehicles meeting criteria

The federal government offers a tax credit for used electric vehicles (EVs) to make the transition to electric mobility more affordable for a broader range of consumers. Under the Used EV Credit program, eligible buyers can receive up to $4,000 as a tax credit when purchasing a pre-owned electric vehicle that meets specific criteria. This credit is part of the broader effort to reduce greenhouse gas emissions and promote sustainable transportation. Unlike the new EV tax credit, which is applied at the point of sale, the used EV credit is claimed when filing federal taxes, reducing the taxpayer’s liability dollar-for-dollar.

To qualify for the Used EV Credit, the vehicle must meet several requirements. First, the EV must be at least two years old at the time of purchase, as the credit is specifically designed for pre-owned vehicles. Second, the vehicle’s model year must be eligible under the current tax credit guidelines, which are updated periodically. Third, the buyer’s modified adjusted gross income (MAGI) must fall below certain thresholds, as the credit phases out for higher-income individuals. Finally, the vehicle must have a battery capacity of at least 7 kilowatt-hours (kWh) and be acquired for personal use, not for resale.

The $4,000 credit is not automatically granted; it is calculated as 30% of the sale price, up to the maximum limit. For example, if a used EV is purchased for $12,000, the credit would be $3,600 (30% of $12,000), while a $15,000 purchase would qualify for the full $4,000 credit. This structure ensures that the credit is proportional to the cost of the vehicle, making it accessible to buyers of both lower- and higher-priced used EVs. It’s important to note that the credit is non-refundable, meaning it can only reduce the taxpayer’s liability to zero but cannot result in a refund if the credit exceeds the tax owed.

Buyers interested in claiming the Used EV Credit must retain documentation proving eligibility, including the vehicle’s sale price, model year, and battery capacity. IRS Form 8936 is used to claim the credit when filing federal taxes. Additionally, the vehicle must be purchased from a qualified dealer or seller, as private-party sales do not qualify. This credit cannot be combined with the new EV tax credit, so buyers must choose the option that best suits their situation.

The Used EV Credit is particularly beneficial for budget-conscious consumers who want to enter the EV market without the higher cost of a new vehicle. By reducing the effective purchase price of a pre-owned EV, this credit makes electric vehicles more accessible to a wider audience. However, buyers should carefully review the eligibility criteria and consult a tax professional to ensure compliance with IRS rules and maximize their potential savings. This initiative not only supports individual buyers but also contributes to the broader goal of reducing carbon emissions through increased EV adoption.

Understanding Electrical Energy: The Essential Unit of Measurement Explained

You may want to see also

Explore related products

![]()

Claiming Process: IRS Form 8936 filing details for tax credit redemption

To claim the federal tax credit for electric vehicles (EVs), taxpayers must follow a specific process that involves filing IRS Form 8936. This form, titled "Qualified Plug-in Electric Drive Motor Vehicle Credit," is used to calculate and claim the credit for eligible vehicles. The first step in the claiming process is to ensure that the vehicle qualifies for the credit. Generally, the vehicle must be new, have a battery capacity of at least 4 kilowatt-hours, and be acquired for personal use. Once eligibility is confirmed, taxpayers can proceed with the filing process.

When preparing to file Form 8936, taxpayers should gather all necessary documentation, including the vehicle's purchase agreement, VIN (Vehicle Identification Number), and proof of battery capacity. The form itself is divided into several sections, each requiring specific information. Part I of the form asks for details about the vehicle, such as the make, model, and date of purchase. Taxpayers must also indicate whether the vehicle is fully electric or a plug-in hybrid. Part II is where the credit amount is calculated, based on the vehicle's battery capacity and other factors. It's crucial to follow the instructions carefully to ensure accurate calculations.

After completing Parts I and II, taxpayers proceed to Part III, which determines the allowable credit. This section takes into account any limitations, such as the phase-out of the credit for manufacturers that have sold more than 200,000 qualifying vehicles. Taxpayers must refer to the IRS guidelines or consult the manufacturer to confirm if the phase-out applies. Once the allowable credit is determined, it is carried over to the appropriate line on the taxpayer's Form 1040, where it reduces the overall tax liability. If the credit exceeds the tax liability, the excess cannot be refunded but may be carried forward to future tax years.

Filing Form 8936 requires attention to detail and adherence to IRS guidelines. Taxpayers should retain all supporting documents in case of an audit. Additionally, it’s advisable to consult the IRS instructions for Form 8936 or seek assistance from a tax professional to ensure compliance with all requirements. The form must be filed with the taxpayer’s annual tax return for the year in which the vehicle was placed in service. Failure to file the form correctly may result in the denial of the credit.

Lastly, taxpayers should be aware that the electric vehicle tax credit is subject to change based on federal legislation. It’s important to verify the current credit amount and eligibility criteria before filing. By carefully following the instructions for Form 8936 and maintaining thorough records, taxpayers can successfully claim the federal tax credit for their electric vehicles, reducing their tax burden while promoting environmentally friendly transportation.

Understanding the Best Plastic Materials for Electrical Fittings and Components

You may want to see also

Frequently asked questions

The Electric Federal Tax Credit is a financial incentive offered by the U.S. government to encourage the purchase of electric vehicles (EVs). It allows eligible buyers to claim a tax credit of up to $7,500, depending on the vehicle’s battery capacity and other criteria.

Eligibility depends on the vehicle’s specifications, the buyer’s tax liability, and the manufacturer’s sales cap. The credit phases out once a manufacturer sells 200,000 qualifying vehicles. Buyers must also have sufficient tax liability to claim the full credit.

The credit amount is based on the vehicle’s battery capacity, with a base credit of $2,500 plus $417 for each kilowatt-hour (kWh) of battery capacity over 5 kWh, up to a maximum of $7,500. The vehicle must also meet certain requirements, such as being new and primarily used in the U.S.

No, the federal tax credit for electric vehicles only applies to new, qualifying EVs. However, there are separate incentives for used EVs under the Inflation Reduction Act, such as a credit of up to $4,000 for eligible used EV purchases.

To claim the credit, you must file IRS Form 8936 with your federal tax return. The credit reduces your tax liability dollar-for-dollar, but it is non-refundable, meaning it cannot result in a tax refund if your liability is less than the credit amount.