The potential electric car market is vast and rapidly expanding, driven by global efforts to reduce carbon emissions, advancements in battery technology, and increasing consumer awareness of environmental sustainability. With governments worldwide implementing stricter emission regulations and incentives for electric vehicle (EV) adoption, the demand for EVs is expected to surge. Additionally, declining battery costs and improving charging infrastructure are making electric cars more accessible and convenient for consumers. Analysts predict that the EV market could account for a significant portion of global vehicle sales in the coming decades, with some estimates suggesting it could reach tens of millions of units annually by 2030. This growth is further fueled by the entry of major automakers and startups alike, offering a diverse range of electric models to cater to various consumer preferences and price points. As such, the potential electric car market represents not only a transformative shift in the automotive industry but also a pivotal opportunity to address climate change on a global scale.

| Characteristics | Values |

|---|---|

| Global Electric Vehicle (EV) Sales (2023) | ~14 million units (estimated) |

| Market Share of EVs in Global Car Sales (2023) | ~18% |

| Projected Global EV Sales by 2030 | 40-50 million units annually |

| Projected EV Market Share by 2030 | 50-60% of global car sales |

| Largest EV Markets (2023) | China (~60% of global EV sales), Europe (~25%), U.S. (~10%) |

| Government Incentives | Over 50 countries offer subsidies, tax breaks, or purchase grants |

| Charging Infrastructure Growth | Over 3 million public charging stations globally (2023) |

| Battery Cost Reduction | ~$137/kWh in 2023 (down from ~$1,200/kWh in 2010) |

| Consumer Interest | 40-50% of global car buyers consider EVs as their next purchase |

| Corporate Commitments | Major automakers aim for 50-100% EV sales by 2030 (e.g., GM, Volvo, BMW) |

| Environmental Impact | EVs reduce CO2 emissions by 50-70% compared to ICE vehicles (lifecycle) |

| Technological Advancements | Improved range (avg. 300+ miles), faster charging (10-80% in 20-30 mins) |

| Total Addressable Market (TAM) | ~$1 trillion by 2030 (including vehicles, batteries, and infrastructure) |

Explore related products

$37.44 $49.99

$170 $190

What You'll Learn

![]()

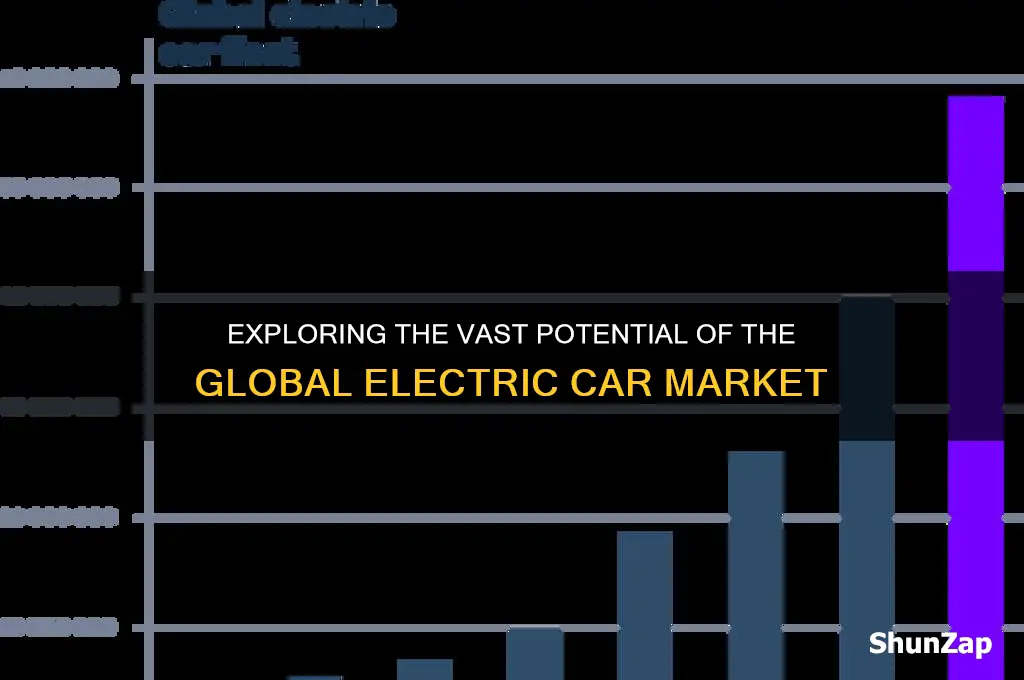

Global EV Sales Projections

The global electric vehicle (EV) market is poised for explosive growth, with projections indicating a seismic shift in automotive sales over the next decade. By 2030, EVs are expected to capture between 40% and 60% of total vehicle sales worldwide, according to reports from BloombergNEF and McKinsey. This surge is driven by declining battery costs, stringent emissions regulations, and increasing consumer demand for sustainable transportation. For context, in 2022, EVs accounted for just 14% of global car sales, highlighting the rapid acceleration anticipated in the coming years.

To understand this growth, consider the regional disparities shaping EV adoption. China, already the largest EV market, is projected to maintain its dominance, with EVs potentially comprising over 50% of its new car sales by 2030. Europe follows closely, with countries like Norway, Germany, and the UK leading the charge, supported by aggressive government incentives and infrastructure investments. Meanwhile, the U.S. market, though slower to adopt, is expected to see a significant uptick as federal policies and charging networks expand. These regional variations underscore the importance of localized strategies for automakers aiming to capitalize on the EV boom.

However, achieving these projections hinges on overcoming critical challenges. One major hurdle is the expansion of charging infrastructure, which must grow exponentially to support millions of new EVs. For instance, the International Energy Agency estimates that the global charging network needs to increase by at least 50-fold by 2030 to meet demand. Additionally, supply chain constraints, particularly for critical materials like lithium and cobalt, could slow production. Automakers and policymakers must collaborate to address these bottlenecks, ensuring a smooth transition to electrification.

Another factor influencing EV sales projections is consumer behavior. Studies show that range anxiety and higher upfront costs remain barriers for many buyers. However, as battery technology improves—with ranges exceeding 300 miles becoming standard—and total cost of ownership parity with internal combustion engine (ICE) vehicles is achieved, these concerns will diminish. Incentives such as tax credits and rebates, like the U.S. Inflation Reduction Act, further sweeten the deal for consumers. By 2025, EVs are expected to reach price parity with ICE vehicles in most markets, making them an increasingly attractive option.

In conclusion, global EV sales projections paint a picture of transformative growth, but realizing this potential requires coordinated efforts across industries and regions. From infrastructure development to consumer education, every stakeholder has a role to play. As the world accelerates toward a sustainable future, the EV market’s size is not just a question of possibility—it’s a matter of inevitability, provided the right steps are taken today.

Hidden Energy Drain: Devices Using Electricity Even When Turned Off

You may want to see also

Explore related products

$12.95 $12.95

![]()

Regional Market Growth Trends

The electric vehicle (EV) market is expanding at varying rates across regions, driven by distinct economic, policy, and cultural factors. In China, the world’s largest EV market, government subsidies, stringent emission regulations, and a robust domestic manufacturing base have propelled growth. By 2023, EVs accounted for over 20% of new car sales in China, with projections suggesting this could reach 40% by 2030. In contrast, Europe has seen rapid adoption due to aggressive carbon neutrality targets, with Norway leading the charge—over 80% of new cars sold there in 2023 were electric. European Union policies, such as the ban on internal combustion engines by 2035, further cement this trend.

In North America, the market is growing steadily but faces challenges like charging infrastructure gaps and higher vehicle costs. The U.S. Inflation Reduction Act, offering up to $7,500 in tax credits for EV purchases, aims to accelerate adoption, but regional disparities persist. California, with its Zero-Emission Vehicle mandate, accounts for nearly half of U.S. EV sales, while other states lag due to lower incentives and consumer awareness. Meanwhile, India is an emerging player, with the government targeting 30% EV penetration by 2030. However, high battery costs, limited charging infrastructure, and consumer skepticism remain barriers, though initiatives like the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme are driving incremental growth.

Southeast Asia presents a mixed picture. Countries like Thailand and Indonesia are leveraging their positions as automotive manufacturing hubs to boost EV production, with Thailand aiming for 30% EV sales by 2030. However, low consumer purchasing power and inadequate infrastructure hinder widespread adoption. In Africa, the market is nascent but holds potential, particularly in South Africa and Morocco, where government incentives and renewable energy integration are beginning to take root. Across these regions, the interplay of policy, infrastructure, and consumer behavior will dictate the pace and scale of EV market growth.

To capitalize on regional trends, stakeholders must tailor strategies to local conditions. In mature markets like China and Europe, focus should shift from adoption to sustainability, such as recycling batteries and expanding fast-charging networks. In developing regions like India and Southeast Asia, affordability and accessibility are key—manufacturers should explore low-cost EV models and public-private partnerships to build charging infrastructure. Policymakers in North America and Africa must address regulatory gaps and incentivize both supply and demand. By aligning efforts with regional specifics, the global EV market can achieve its full potential, estimated at over 50% of new car sales by 2040.

Unlocking Green Mobility: Your Guide to Electric Car Government Grants

You may want to see also

Explore related products

![]()

Consumer Adoption Barriers

Despite the growing buzz around electric vehicles (EVs), their market penetration remains below 10% globally, with significant variations by region. This disparity highlights the persistent consumer adoption barriers that stifle potential growth. One primary obstacle is range anxiety, the fear that an EV’s battery will run out before reaching a charging station. While modern EVs like the Tesla Model S offer ranges exceeding 400 miles, consumer perception lags behind reality. Surveys indicate that 60% of drivers overestimate their weekly driving needs, fueling unnecessary concern. Addressing this requires not just technological improvements but also targeted education campaigns that align consumer expectations with actual usage patterns.

Another critical barrier is the higher upfront cost of EVs compared to traditional internal combustion engine (ICE) vehicles. Even with incentives, the average EV price remains $10,000-$15,000 more than its ICE counterpart. While total cost of ownership (TCO) calculations often favor EVs due to lower fuel and maintenance costs, consumers remain price-sensitive at the point of purchase. Financial institutions can play a pivotal role here by offering tailored loan products with lower interest rates for EVs, coupled with government subsidies that reduce the initial burden. For instance, Norway’s success in achieving 80% EV sales by 2022 was driven by substantial tax exemptions and infrastructure investments.

The charging infrastructure gap further complicates adoption, particularly in suburban and rural areas. Urban dwellers may have access to over 100,000 public charging stations in the U.S. alone, but rural residents face a starkly different reality. A McKinsey study found that 70% of rural households lack access to nearby charging options, making EV ownership impractical. Bridging this gap requires strategic investments in fast-charging networks along highways and in underserved communities. Employers and multifamily housing developers can also contribute by installing workplace and residential chargers, reducing reliance on public infrastructure.

Lastly, consumer skepticism about battery technology persists, particularly regarding longevity and environmental impact. While EV batteries are designed to retain 70-80% capacity after 10 years, misconceptions about frequent replacements deter buyers. Additionally, the carbon footprint of battery production raises ethical concerns, though lifecycle analyses show EVs emit 50% less CO2 than ICE vehicles over their lifespan. Manufacturers can alleviate these concerns through transparent reporting on battery recycling programs and partnerships with renewable energy suppliers. For instance, Volkswagen’s commitment to using 100% green energy in battery production sets a benchmark for industry accountability.

Overcoming these barriers requires a multifaceted approach, blending policy intervention, industry innovation, and consumer education. By addressing range anxiety, cost disparities, infrastructure limitations, and technological skepticism, stakeholders can unlock the full potential of the electric car market. The transition to EVs is not just a technological shift but a cultural one, demanding collaboration across sectors to reshape consumer behavior and drive sustainable mobility.

Scooters and the Law: Electric Vehicles or Not?

You may want to see also

Explore related products

![]()

Charging Infrastructure Expansion

The rapid growth of the electric vehicle (EV) market hinges on the expansion of charging infrastructure, a critical factor that can either accelerate adoption or stifle it. By 2030, projections suggest that over 145 million EVs could be on the road globally, but this potential market size is contingent on addressing the "range anxiety" that deters many consumers. Charging infrastructure must not only expand in quantity but also in strategic placement, ensuring accessibility in urban centers, highways, and rural areas alike. Without a robust network, even the most advanced EVs will struggle to compete with the convenience of traditional gasoline vehicles.

Consider the analogy of smartphones and Wi-Fi: just as widespread internet access fueled smartphone adoption, a dense and reliable charging network is essential for EVs. Governments and private companies must collaborate to deploy Level 2 chargers in residential areas, DC fast chargers along highways, and workplace charging stations to cater to daily commuting needs. For instance, the U.S. Infrastructure Investment and Jobs Act allocates $7.5 billion for EV charging, aiming to build a national network of 500,000 chargers by 2030. Such initiatives are not just investments in infrastructure but in consumer confidence, reducing barriers to EV ownership.

However, expansion alone is insufficient; interoperability and standardization are equally vital. Imagine a scenario where an EV owner cannot charge at a station due to incompatible connectors or payment systems—a frustrating experience that could deter future use. To avoid this, industry stakeholders must adopt universal standards, such as the Combined Charging System (CCS) in Europe and North America, ensuring seamless access across networks. Additionally, integrating renewable energy sources into charging stations can enhance sustainability, appealing to environmentally conscious consumers and aligning with global decarbonization goals.

A practical tip for policymakers and businesses is to prioritize data-driven planning. Analyzing traffic patterns, population density, and existing fuel station locations can identify optimal sites for chargers. For example, placing fast chargers at rest stops every 50 miles on major highways can alleviate range anxiety for long-distance travelers. Similarly, incentivizing businesses to install chargers in parking lots can cater to employees and customers, fostering a culture of convenience. By combining strategic deployment with technological innovation, charging infrastructure expansion can unlock the full potential of the electric car market.

Exploring the Blazing Speed of 2S Electric Touring Cars

You may want to see also

Explore related products

![]()

Government Policy Impacts

Government incentives and regulations are pivotal in shaping the electric vehicle (EV) market, often determining its growth trajectory. For instance, countries like Norway, where EVs accounted for over 80% of new car sales in 2022, have implemented aggressive policies such as tax exemptions, toll discounts, and free public charging. These measures not only reduce the upfront cost of EVs but also enhance their operational convenience, making them a more attractive option than traditional internal combustion engine (ICE) vehicles. Conversely, regions with minimal or inconsistent policies, like parts of the U.S. outside California, often lag in EV adoption, highlighting the direct correlation between government action and market size.

To maximize the impact of EV policies, governments must adopt a multi-faceted approach. First, subsidies and tax credits should be structured to target middle-income consumers, who are often the largest untapped market segment. For example, a tiered incentive system could offer higher rebates for households earning below $75,000 annually, ensuring affordability without disproportionately benefiting high-income buyers. Second, infrastructure investment is critical. A study by the International Energy Agency (IEA) suggests that for every $1 spent on EV subsidies, $2 should be allocated to charging networks to address range anxiety, a persistent barrier to adoption.

However, policy design must also account for potential pitfalls. Phase-out strategies for incentives are essential to avoid market dependency. For instance, the U.S. federal EV tax credit begins phasing out once a manufacturer sells 200,000 qualifying vehicles, encouraging early adoption while preventing long-term reliance on subsidies. Additionally, regulatory mandates, such as the European Union’s ban on ICE vehicle sales by 2035, provide long-term certainty for automakers and consumers alike, fostering innovation and investment in EV technology.

A comparative analysis reveals that the most successful EV markets combine carrot-and-stick approaches. China, the world’s largest EV market, employs strict emissions standards alongside generous subsidies, driving both supply and demand. In contrast, Germany’s focus on subsidies alone has yielded slower growth, underscoring the need for balanced policies. Governments should also leverage data-driven adjustments, such as monitoring regional adoption rates and adjusting incentives accordingly, to ensure equitable market expansion.

Ultimately, the potential size of the EV market is not solely determined by consumer preferences or technological advancements but by the strategic deployment of government policies. By crafting targeted, adaptable, and comprehensive measures, policymakers can accelerate the transition to electric mobility, unlocking a market projected to reach $800 billion by 2027. The key lies in understanding that policy is not just a tool for market stimulation but a blueprint for sustainable transformation.

Windmill Electricity in Homes: A Historical Shift to Renewable Energy

You may want to see also

Frequently asked questions

The potential global electric car market is projected to reach tens of millions of units annually by 2030, with estimates ranging from 20 to 40 million vehicles per year, driven by declining battery costs, stricter emissions regulations, and increasing consumer demand.

Key drivers include government incentives and subsidies, advancements in battery technology, rising fuel prices, environmental concerns, and the expanding charging infrastructure network.

China, Europe, and North America are currently the largest markets, but emerging economies in Asia, Latin America, and Africa also hold significant potential as infrastructure and affordability improve.

The electric car market is expected to grow exponentially, potentially surpassing the ICE market by the mid-2030s, as more countries announce bans on fossil fuel vehicles and automakers shift their focus to electrification.