The global automotive industry is undergoing a transformative shift towards electrification, prompting a critical examination of how much of the car market is electric. As of recent data, electric vehicles (EVs) account for approximately 10-15% of total new car sales worldwide, with significant variations across regions. Countries like Norway, where EVs dominate with over 80% market share, contrast sharply with emerging markets where adoption remains in the single digits. This disparity is driven by factors such as government incentives, charging infrastructure availability, and consumer awareness. With major automakers committing to electric futures and governments setting ambitious targets to phase out internal combustion engines, the electric share is projected to grow exponentially, potentially reaching 50% or more by 2030. This rapid evolution underscores the pivotal role EVs play in shaping the future of transportation and addressing climate concerns.

| Characteristics | Values |

|---|---|

| Global Electric Vehicle (EV) Market Share (2023) | ~14% (includes Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs)) |

| Largest EV Market by Region (2023) | China (approximately 60% of global EV sales) |

| Second Largest EV Market by Region (2023) | Europe (around 25% of global EV sales) |

| Third Largest EV Market by Region (2023) | United States (approximately 10% of global EV sales) |

| Fastest Growing EV Market (2023) | Europe (with several countries exceeding 20% EV market share) |

| Country with Highest EV Market Share (2023) | Norway (over 80% of new car sales are electric) |

| Global BEV Sales (2023) | ~10 million units |

| Global PHEV Sales (2023) | ~3 million units |

| Projected Global EV Market Share by 2030 | 30-40% (varies by region and policy) |

| Key Drivers of EV Adoption | Government incentives, declining battery costs, and environmental regulations |

| Average Battery Cost (2023) | ~$137 per kWh (down from ~$1,200 per kWh in 2010) |

| Charging Infrastructure Growth (2023) | Over 2.7 million public charging points globally |

| Corporate Commitments | Many automakers aim for 50-100% EV sales by 2030 (e.g., Volvo, GM) |

Explore related products

What You'll Learn

![]()

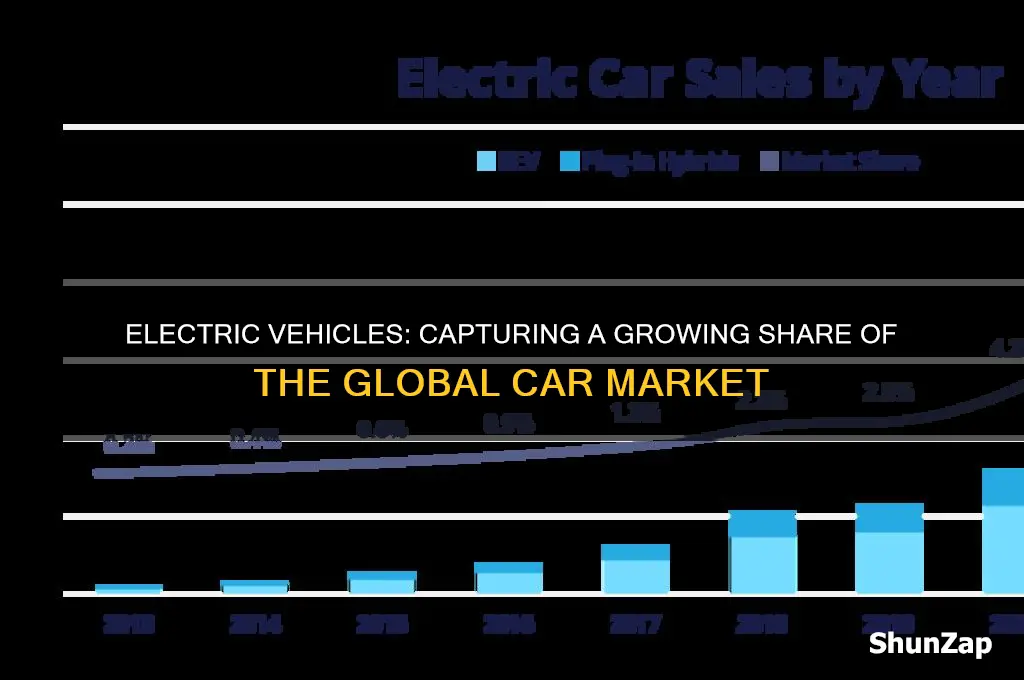

Global EV Sales Growth

Electric vehicles (EVs) are no longer a niche market but a rapidly expanding segment of the global automotive industry. In 2022, EV sales accounted for approximately 14% of the total car market, a significant leap from just 4% in 2019. This growth is not uniform across regions; China leads the charge, with EVs representing over 25% of new car sales, followed by Europe at around 20%. North America lags behind at roughly 7%, though recent policy shifts and infrastructure investments suggest accelerating adoption. These disparities highlight the influence of government incentives, charging infrastructure, and consumer preferences on EV penetration.

To understand the drivers of this growth, consider the role of policy and innovation. Governments worldwide are tightening emissions regulations, with the European Union aiming to phase out internal combustion engine (ICE) vehicles by 2035. Simultaneously, technological advancements have reduced battery costs by 89% since 2010, making EVs more affordable. For instance, the average price of a mid-range EV has dropped from $45,000 to $35,000 in the past five years. Manufacturers are also expanding their EV lineups; Tesla, BYD, and Volkswagen now offer models across price points, catering to diverse consumer needs.

However, challenges remain. Range anxiety persists, despite the average EV now offering over 250 miles on a single charge. Charging infrastructure is still inadequate in many regions, with rural areas particularly underserved. For example, the U.S. has only 1 charging station per 40 EVs, compared to 1 per 15 in Europe. Addressing this gap requires strategic investment, with governments and private companies collaborating to deploy fast-charging networks. Consumers can mitigate this issue by installing home chargers, which cost $500–$1,200, and leveraging apps like PlugShare to locate public stations.

A comparative analysis reveals that EV adoption is not just about technology but also cultural shifts. In Norway, where EVs constitute 80% of new car sales, success stems from aggressive incentives: zero VAT, free public parking, and access to bus lanes. Contrast this with Australia, where EVs make up only 3% of sales, due to high import taxes and limited government support. This underscores the importance of holistic strategies that combine policy, infrastructure, and consumer education to drive growth.

Looking ahead, the trajectory of global EV sales growth is clear but not without hurdles. By 2030, EVs are projected to capture 40–50% of the global car market, fueled by declining costs, expanding models, and stricter regulations. However, achieving this requires addressing supply chain bottlenecks, particularly in battery materials like lithium and cobalt. Automakers and policymakers must also prioritize sustainability, ensuring that EV production minimizes environmental impact. For consumers, the takeaway is straightforward: EVs are no longer the future—they are the present, and the time to transition is now.

Cold Weather Impact: How Electric Cars Perform in Low Temperatures

You may want to see also

Explore related products

![]()

Regional Market Penetration Rates

Electric vehicle adoption varies dramatically by region, driven by policy, infrastructure, and consumer preferences. In Europe, EVs claimed 21% of new car sales in 2023, with Norway leading at 86% penetration—a result of aggressive tax incentives, free charging, and toll exemptions. Germany and France follow with 17% and 15% respectively, buoyed by subsidies like Germany’s *Umweltbonus* (€6,750 per EV). In contrast, China dominates global EV sales, capturing 60% of the world’s total, yet its domestic penetration is 30%, fueled by mandates for automakers to meet EV quotas and a robust battery supply chain. Meanwhile, the United States lags at 7% penetration, despite the Inflation Reduction Act’s $7,500 tax credit, hindered by higher gasoline prices and slower charging infrastructure rollout.

To understand these disparities, consider the interplay of policy and infrastructure. Regions with higher penetration rates often have stricter emissions regulations, direct purchase incentives, and widespread charging networks. For instance, the EU’s 2035 ban on internal combustion engines accelerates EV adoption, while China’s Battery-as-a-Service model reduces upfront costs. Conversely, in the U.S., fragmented state policies and a reliance on federal initiatives slow progress. For policymakers, the takeaway is clear: combine mandates with incentives and infrastructure investment to drive adoption.

A comparative analysis reveals that Asia-Pacific (excluding China) shows mixed results. South Korea and Japan have penetration rates of 12% and 8%, respectively, with Hyundai and Nissan leading local efforts. However, India lags at 1%, despite ambitious targets, due to high battery costs and limited charging stations. In Latin America, Chile stands out with 10% penetration, thanks to tax exemptions and renewable energy integration, while Brazil remains below 1%, constrained by ethanol’s dominance and weak policy support.

For consumers, regional trends offer practical insights. In high-penetration markets like Europe, leasing EVs is often more cost-effective than buying, given rapid battery depreciation. In the U.S., focus on states like California or New York, where additional rebates (up to $2,000) and denser charging networks improve ownership viability. In emerging markets, consider hybrid vehicles as a transitional step, as seen in India’s push for hybrid buses.

Ultimately, regional penetration rates highlight the importance of tailored strategies. While Europe and China lead through policy and manufacturing scale, the U.S. and developing markets require targeted interventions to overcome barriers. By studying these variations, stakeholders can replicate successes and avoid pitfalls, accelerating the global shift to electric mobility.

NASA's Electric Space Vehicles: Fact or Fiction?

You may want to see also

Explore related products

![]()

Government Incentives Impact

Government incentives have become a pivotal force in accelerating the adoption of electric vehicles (EVs), reshaping the automotive market in measurable ways. By offering financial rebates, tax credits, and reduced registration fees, governments effectively lower the upfront cost barrier that often deters consumers from transitioning to EVs. For instance, in the United States, the federal tax credit of up to $7,500 for qualifying electric vehicles has significantly influenced purchasing decisions, with states like California and New York adding their own incentives to further sweeten the deal. This layered approach not only makes EVs more affordable but also signals a long-term commitment to sustainable transportation.

However, the impact of these incentives isn’t uniform across regions or demographics. In Norway, where EVs accounted for over 80% of new car sales in 2022, a combination of exemptions from import taxes, VAT, and road tolls has created an unparalleled market shift. Contrast this with countries like India, where despite the introduction of the FAME II scheme offering subsidies of up to ₹1.5 lakh for electric two-wheelers and cars, EV adoption remains sluggish due to limited charging infrastructure and consumer awareness. This disparity highlights that while incentives are powerful, their success hinges on complementary policies and infrastructure development.

To maximize the effectiveness of government incentives, policymakers must adopt a strategic, multi-faceted approach. First, incentives should be tiered based on vehicle efficiency and battery capacity, rewarding consumers for choosing models with longer ranges and lower environmental footprints. Second, age-based incentives, such as higher rebates for first-time EV buyers under 30, could engage younger demographics more actively in the green transition. Lastly, governments should pair financial incentives with mandates for workplace and public charging stations, addressing range anxiety—a persistent psychological barrier to EV adoption.

Critics argue that such incentives disproportionately benefit wealthier consumers who can afford new vehicles, but data suggests otherwise. In regions like British Columbia, where low-income households receive an additional $2,500 rebate on top of the standard $3,000 incentive, EV ownership among lower-income groups has risen by 15% since 2020. This demonstrates that with targeted design, incentives can democratize access to clean transportation. The takeaway is clear: government incentives are not just a cost but an investment in reducing emissions, improving public health, and fostering innovation in the automotive sector. When crafted thoughtfully, they can catalyze a market transformation that benefits society at large.

Household Appliances Powered by AC Electricity: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Battery Technology Advancements

As of 2023, electric vehicles (EVs) account for approximately 14% of the global car market, with projections suggesting this figure could surpass 50% by 2030. This rapid growth is fueled by advancements in battery technology, which address key consumer concerns such as range anxiety, charging times, and cost. Among these innovations, improvements in energy density, solid-state batteries, and recycling methods stand out as pivotal drivers of EV adoption.

Consider energy density, a critical factor in determining an EV’s range. Modern lithium-ion batteries achieve around 250–300 watt-hours per kilogram (Wh/kg), but next-generation technologies like lithium-sulfur and silicon-anode batteries promise to push this to 400–500 Wh/kg. For consumers, this translates to vehicles like the Lucid Air, which already boasts a 520-mile range on a single charge. To maximize battery life, avoid frequent fast charging and maintain the charge level between 20% and 80%, as extreme states accelerate degradation.

Solid-state batteries represent another leap forward, replacing liquid electrolytes with solid materials to enhance safety, energy density, and charging speed. Toyota and QuantumScape are leading the charge, with prototypes claiming 15-minute charging times and double the range of current EVs. While not yet commercially available, these batteries could revolutionize long-distance travel, making EVs as convenient as gasoline cars. Until then, drivers can optimize their current EV experience by using apps like PlugShare to locate fast-charging stations along their routes.

Recycling advancements are equally transformative, addressing the environmental impact of battery production. Companies like Redwood Materials recover up to 95% of critical materials like cobalt, nickel, and lithium from spent batteries, reducing reliance on mining. For EV owners, participating in manufacturer take-back programs ensures responsible disposal and supports a circular economy. Additionally, choosing EVs with longer warranties (e.g., Tesla’s 8-year battery coverage) provides peace of mind regarding longevity and sustainability.

In summary, battery technology advancements are not just enhancing EV performance but also reshaping the automotive industry’s future. By focusing on energy density, solid-state innovations, and recycling, these developments address practical barriers to adoption, making electric vehicles a viable option for a broader audience. As these technologies mature, the question shifts from “how much of the car market is electric?” to “how soon will it dominate?”

The Best Places to Buy Electric Vehicles

You may want to see also

Explore related products

![LISEN Magnetic Phone Holder for Car, MagSafe Car Mount for iPhone 17 Car Accessories for Men Women Gifts for Christmas [95% Increase Magnet] Car Vent Phone Mount RV Truck Mat Fit GPS iPhone 17 Pro Max](https://m.media-amazon.com/images/I/81z73-rH4hL._AC_UL320_.jpg)

![]()

Charging Infrastructure Expansion

As of 2023, electric vehicles (EVs) account for approximately 14% of global car sales, with projections suggesting this figure could reach 50% by 2030. This rapid growth underscores the urgency of expanding charging infrastructure to support widespread adoption. Without a robust and accessible charging network, the transition to electric mobility risks stagnation, leaving consumers hesitant to abandon internal combustion engines.

Consider the disparity in charging availability: while urban areas often boast multiple fast-charging stations, rural regions frequently lack even basic Level 2 chargers. This imbalance creates a two-tiered system where EV ownership is feasible for some but impractical for others. To address this, governments and private companies must collaborate to deploy chargers in underserved areas, prioritizing locations along major highways and in remote communities. Incentives such as tax credits or grants can encourage investment in these regions, ensuring equitable access to charging resources.

Expanding infrastructure isn’t just about quantity—it’s also about quality and compatibility. The current landscape is fragmented, with competing standards like CCS, CHAdeMO, and Tesla’s proprietary system. This fragmentation frustrates drivers and slows adoption. Standardization efforts, such as the EU’s push for CCS as the universal standard, are critical. Manufacturers and policymakers must align on a single protocol to streamline the user experience and reduce costs.

Another key aspect is integrating charging infrastructure with renewable energy sources. Pairing EV chargers with solar panels or wind turbines not only reduces the carbon footprint of charging but also provides a selling point for environmentally conscious consumers. For instance, installing solar-powered chargers in parking lots or along highways can turn idle spaces into energy-generating hubs. Businesses can leverage this approach to attract customers while contributing to sustainability goals.

Finally, innovation in charging technology will play a pivotal role in scaling infrastructure. Wireless charging, for example, offers a glimpse into a future where EVs charge seamlessly while parked. Pilot projects in cities like Oslo and Seoul demonstrate its potential, though widespread adoption requires overcoming technical and cost barriers. Similarly, ultra-fast chargers capable of delivering 200+ kW can reduce charging times to under 20 minutes, rivaling the convenience of refueling conventional vehicles. Investing in such advancements will be essential to meet the demands of a growing EV market.

Understanding Kenya's Electrical Plug Types: A Comprehensive Guide for Travelers

You may want to see also

Frequently asked questions

As of 2023, electric vehicles (EVs) account for approximately 14% of the global car market, with significant regional variations.

Norway leads the world with over 80% of new car sales being electric vehicles, largely due to government incentives and infrastructure support.

In the United States, electric vehicles make up about 7-8% of new car sales as of 2023, with growth accelerating due to policy initiatives and expanding charging networks.

In Europe, electric vehicles represent around 20% of new car sales, driven by strict emissions regulations and strong consumer demand in countries like Germany and France.

Yes, the electric car market is growing rapidly. Projections suggest EVs could account for 40-50% of global new car sales by 2030, depending on policy support and technological advancements.