Utility companies, including electric companies, often run credit checks on new customers to assess their bill payment history and determine whether to approve their application. A bad credit score is considered a risk by utility officials, and people with low credit scores may be charged a higher deposit for utility services. This deposit acts as an insurance policy for the company in case the customer is delinquent on their payments. While utility companies won't deprive you of services if you have bad credit, they may require a deposit or offer prepaid plans that don't require a credit check.

| Characteristics | Values |

|---|---|

| Credit check | A soft credit check is usually performed by utility companies to review bill payment history. |

| Credit score | A low credit score is considered a risk by utility companies. |

| Deposit | Utility companies may charge a security deposit to hedge against the risk of non-payment. |

| Delinquent accounts | Utility companies may deny service if you have a history of delinquent accounts. |

| Bill payment history | Utility companies examine bill payment history to determine whether to approve an application. |

| Timely payments | On-time utility payments may not improve your credit score, but late payments can negatively impact it. |

| Credit report | Utility companies may request a credit report with permission. |

Explore related products

What You'll Learn

![]()

Credit checks

A utility company must obtain your permission to check your credit report. Typically, when you fill out an application for utility service, you are granting them permission to review your credit report as part of its approval process. If you do not wish to have a credit check, there are alternative options. For example, you may be able to obtain a credit reference letter from another utility company that outlines your service and payment history. Another option is to request a prepaid utility plan that requires no credit check or deposit.

It is important to note that utility companies cannot deny your application solely based on a low credit score. Under most state laws, utility providers must provide service to customers who are willing to pay. However, they may require a deposit, which acts as an insurance policy against delinquent payments. The amount of the deposit can vary, typically ranging from $100 to $250, but it may be higher if you have an outstanding balance with a previous utility company.

If you are concerned about the impact of credit checks on your score, it is worth noting that utility companies usually perform a soft credit check, which does not affect your score. Additionally, most utility companies do not report your bill payment activity to the major credit bureaus (Experian, TransUnion, and Equifax). However, delinquent payments can negatively impact your score, and if the debt is turned over to a collection agency, it may appear on your credit report.

To avoid or reduce the impact of a low credit score, you can focus on improving your score. This can be done by settling delinquent accounts and making timely payments. Reviewing your credit report for errors and disputing any irregularities can also help boost your score.

The Best Day to Switch Electric Companies

You may want to see also

Explore related products

![]()

Deposits

Utility companies, including electric companies, consider a bad credit score as a risk. To hedge against the possibility of customers not paying their bills on time, companies may charge a deposit. This deposit acts as an insurance policy for the company. The amount of the deposit can range from $100 to $250, and it may be higher if you have a low credit score or an outstanding balance with a previous utility company.

Most deregulated power companies in Texas require a deposit in case of delinquency or non-payment of electric bills. However, some electric companies in Texas, such as Quick Electricity, do not require a credit check or deposit for their pay-as-you-go light service. Prepaid utility plans are another option to avoid deposits and credit checks. By paying ahead for power, you can not only skip the credit check but also avoid various fees, including disconnection penalties.

If you choose a fixed-rate electricity plan, you will likely need to agree to a credit verification. A FICO credit score of over 620 will usually be enough to get approved for energy services.

While utility companies may charge a deposit for customers with low credit scores, they cannot deny your application solely based on a poor credit score. Under most state laws, utility providers must provide service to anyone willing to pay for it. However, they can deny service if you have a history of delinquent accounts.

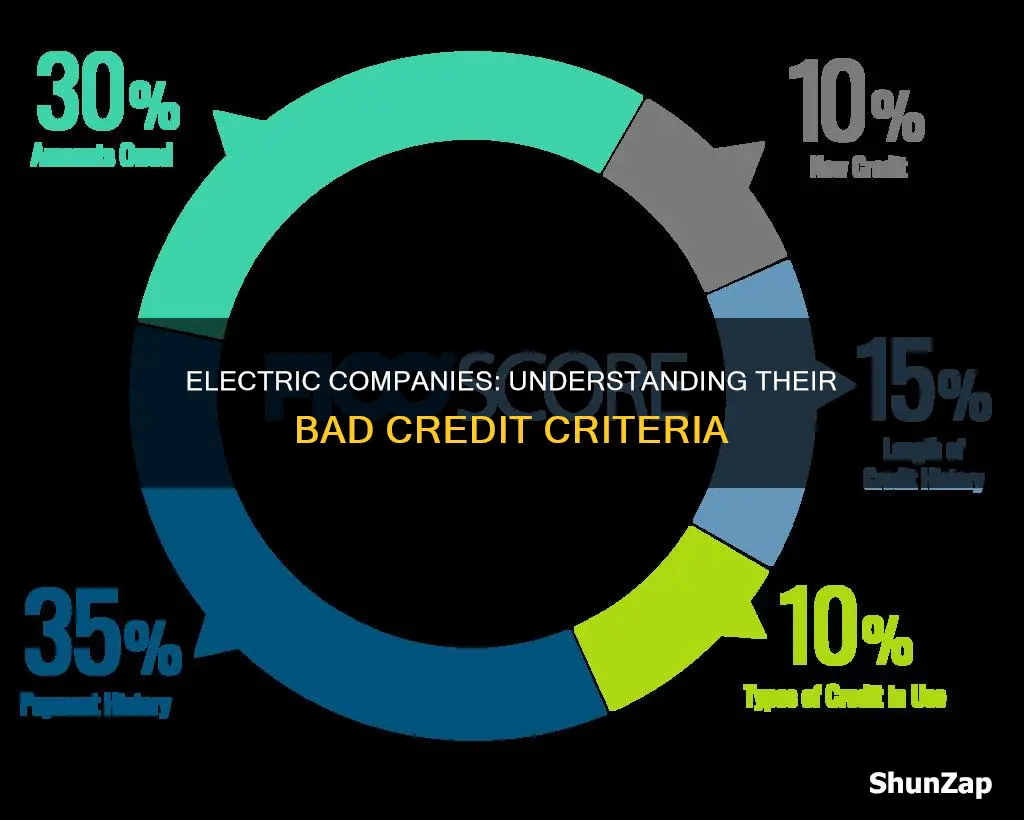

To avoid or reduce the deposit amount, you can work on improving your credit score. This can be done by settling delinquent accounts and making timely payments. Remember that timely payments make up 35% of your overall credit score assessment. Reviewing your credit report for any errors or irregularities and disputing any inaccuracies can also help boost your score.

Edison Electric Light Company: Illuminating the World

You may want to see also

Explore related products

![]()

Payment history

Lenders and creditors will assess your payment history to gauge your likelihood of repaying debts. Consistent on-time payments reflect positively on your creditworthiness, indicating a lower risk of default. Conversely, late, missed, or delinquent payments can negatively impact your credit score and be seen as a red flag by lenders.

Maintaining a solid payment history can be achieved through several strategies:

- Paying bills on time: This is the most critical factor in maintaining a good payment history. Setting up automatic payments or creating a budget to ensure timely bill payments can help keep your credit history positive.

- Getting current on missed payments: While older late payments have a lesser impact on your credit score, consistently paying your bills on time moving forward can help rehabilitate your payment history over time.

- Contacting creditors: If you're struggling with debt, reach out to your creditors to discuss potential options, such as lowering your interest rate or consolidating your debts.

- Seeking credit counselling: Credit counselling services can provide guidance on budgeting and debt management, helping you improve your payment history.

- Enrolling in programs: Programs like Experian Boost can help incorporate your history of utility, cellphone, and streaming service payments into your credit report, boosting your score by recognizing on-time payments.

When it comes to electric companies, a bad credit score may not result in a denial of service, but it can lead to additional costs and requirements. Electric companies may charge a deposit or security deposit for customers with low credit scores to hedge against the risk of non-payment. This deposit can range from $100 to $250 or even more for a house. Prepaid or pay-as-you-go electricity plans may be an option to avoid credit checks, but they often come with additional fees. Improving your credit score before applying for electric services can help you avoid these potential costs and hassles.

Electric Company: What's in a Name for Canadians?

You may want to see also

Explore related products

![]()

Credit scores

Utility companies, including electricity providers, typically conduct credit checks on new customers to assess their bill payment history and determine whether to approve their applications. While a soft credit check may not impact an individual's credit score, it provides utility companies with insights into their payment behaviour. This information is particularly valuable to electricity suppliers as they extend credit to customers by providing services before receiving payment.

A low credit score or a history of delinquent payments can result in higher security deposits being charged by utility companies. These deposits serve as a form of insurance for the company, protecting them from potential financial losses if the customer fails to pay their bills. The amount of these deposits can vary, typically ranging from $100 to $250 or more, depending on the type of residence.

However, it is important to note that utility companies cannot deny services based solely on a low credit score. Under most state laws, utility providers are obligated to supply services to individuals who are willing to pay for them. Additionally, making timely utility payments may not significantly improve one's credit score, but delinquent payments can negatively impact it.

To improve their chances of obtaining electricity services with a bad credit score, individuals can consider the following options:

- Opting for prepaid electricity plans: Some electricity companies offer pay-as-you-go plans that do not require credit checks or deposits.

- Choosing flexible billing options: Selecting an electricity company that provides flexible billing options, such as smaller, more frequent payments, can help establish good credit over time.

- Improving credit scores: Raising a credit score can be achieved through settling delinquent accounts and making timely payments. This may take one to two months or longer, depending on the individual's credit profile.

Westinghouse Electric Company: Powering the World with Innovation

You may want to see also

Explore related products

![]()

Utility bills

Some utility companies run credit checks on new customers to determine whether to approve their application. This is known as a soft credit check or soft inquiry, which does not affect your credit score. They will look at your payment history with other utility companies and your overall score to assess your payment history.

If you have a low credit score or no credit, the utility company may charge you a security deposit, which acts as insurance in case you don't pay your bill. The amount of this deposit can vary, ranging from $100 to $250, and may be higher if you have an outstanding balance with a previous utility company.

You can avoid or reduce the security deposit by improving your credit score. This can be done by settling delinquent accounts and making timely payments. In some cases, you may be able to opt for a prepaid utility plan that requires no credit check or deposit.

It is important to note that while timely utility bill payments are less likely to improve your credit score, late payments can negatively impact it.

Frequently asked questions

Electric companies consider a bad credit score to be a risk and will often require a deposit from customers with low credit scores. While there is no exact figure, this deposit can range from $100 to $250.

Electric companies run credit checks on new customers to see their bill payment history and determine whether to approve their application. This is known as a soft credit check, which doesn't affect your credit score. They will look at your payment history with other utility companies and your overall score.

You can avoid paying a deposit by improving your credit score. This can be done by settling delinquent accounts and making timely payments. You can also choose an electric company with flexible billing options, allowing you to make smaller, more frequent payments to avoid expensive monthly bills.