The market for electric cars has experienced exponential growth over the past decade, driven by advancements in technology, increasing environmental concerns, and supportive government policies. As consumers become more aware of the benefits of electric vehicles (EVs), such as reduced emissions, lower operating costs, and improved performance, demand has surged globally. Major automakers are investing heavily in EV production, expanding their portfolios to cater to diverse preferences, from compact city cars to luxury SUVs. Additionally, the development of charging infrastructure and incentives like tax credits and subsidies are further accelerating adoption. With countries setting ambitious targets to phase out internal combustion engines, the electric car market is poised to become a dominant force in the automotive industry, reshaping mobility and sustainability for the future.

Explore related products

$8.98

$37.18 $49.99

What You'll Learn

- Consumer Demand Trends: Analyzing growth in electric vehicle (EV) adoption and buyer preferences globally

- Government Incentives: Exploring subsidies, tax breaks, and policies promoting EV purchases

- Charging Infrastructure: Assessing availability and expansion of EV charging stations worldwide

- Competitive Landscape: Examining key players, market share, and emerging EV manufacturers

- Technological Advancements: Impact of battery tech, range improvements, and autonomous features on EV market

![]()

Consumer Demand Trends: Analyzing growth in electric vehicle (EV) adoption and buyer preferences globally

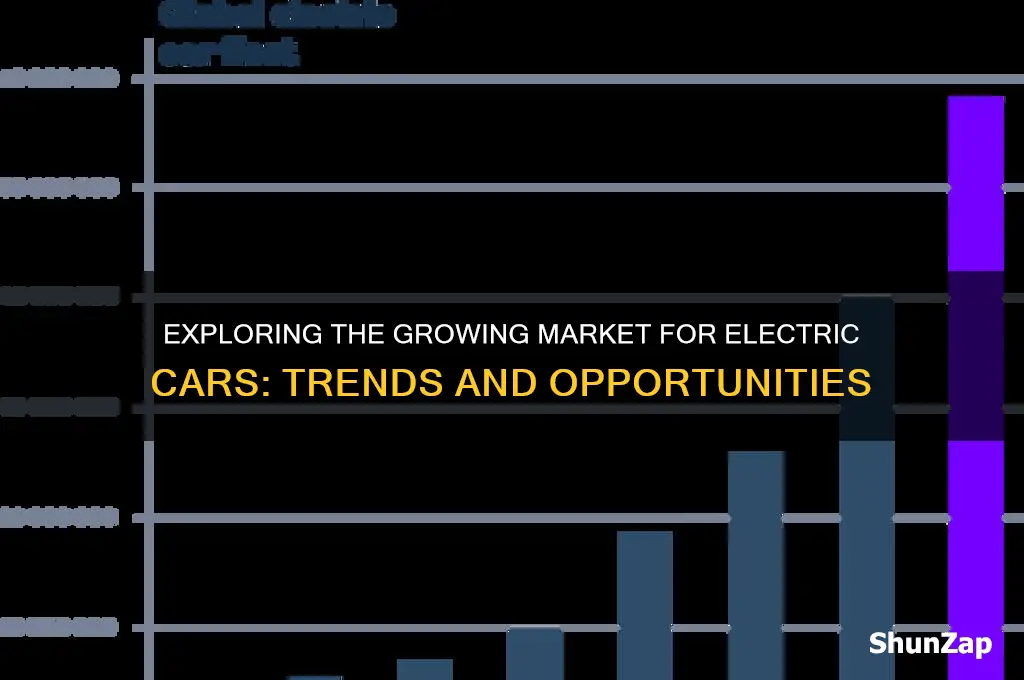

The global electric vehicle (EV) market is experiencing unprecedented growth, with consumer demand surging across diverse regions. In 2023, EV sales surpassed 10 million units worldwide, a 55% increase from the previous year, according to the International Energy Agency (IEA). This acceleration is driven by a combination of factors, including government incentives, declining battery costs, and heightened environmental awareness. However, the pace of adoption varies significantly by region, with China leading the charge, accounting for over 60% of global EV sales, followed by Europe and North America. This disparity highlights the importance of localized strategies to tap into emerging markets.

To understand buyer preferences, consider the shift in consumer priorities. Range anxiety, once a primary concern, is diminishing as battery technology improves, with many EVs now offering over 300 miles on a single charge. Instead, buyers are increasingly focused on charging infrastructure accessibility and vehicle affordability. For instance, a survey by Deloitte revealed that 63% of consumers would be more likely to purchase an EV if charging stations were as ubiquitous as gas stations. Additionally, younger demographics, particularly millennials and Gen Z, prioritize sustainability and tech-savvy features, such as advanced driver-assistance systems (ADAS) and seamless smartphone integration. These preferences underscore the need for automakers to align product offerings with evolving consumer expectations.

A comparative analysis of regional trends reveals distinct patterns in EV adoption. In Europe, stringent emissions regulations and generous subsidies have fueled demand, with Norway achieving an 80% EV market share in 2023. Conversely, the U.S. market, while growing, remains constrained by higher upfront costs and a fragmented charging network. Emerging markets like India and Southeast Asia present untapped potential, but affordability remains a barrier, with EVs often priced 2-3 times higher than their internal combustion engine (ICE) counterparts. To bridge this gap, innovative business models, such as battery-as-a-service (BaaS) and second-life battery applications, are gaining traction, offering cost-effective solutions for price-sensitive consumers.

Persuasively, automakers must adapt to these trends by prioritizing customization and sustainability. For example, Tesla’s success can be attributed to its focus on performance, design, and a robust charging ecosystem. Similarly, legacy manufacturers like Volkswagen and GM are investing heavily in EV platforms, with plans to launch over 30 new models by 2025. However, simply producing EVs is not enough; companies must also address supply chain challenges, such as securing critical materials like lithium and cobalt. By integrating circular economy principles, such as recycling and reusing battery components, automakers can enhance sustainability while reducing costs, thereby appealing to environmentally conscious consumers.

In conclusion, analyzing consumer demand trends in the EV market requires a multifaceted approach. By understanding regional disparities, shifting buyer preferences, and emerging business models, stakeholders can navigate this dynamic landscape effectively. Practical steps include investing in charging infrastructure, leveraging data analytics to tailor marketing strategies, and fostering partnerships to address supply chain bottlenecks. As the world accelerates toward electrification, those who align with consumer needs and innovate proactively will lead the charge in this transformative industry.

Electric Car Running Costs: Unlocking Affordable and Eco-Friendly Driving

You may want to see also

Explore related products

![]()

Government Incentives: Exploring subsidies, tax breaks, and policies promoting EV purchases

Governments worldwide are deploying a variety of financial incentives to accelerate the adoption of electric vehicles (EVs), recognizing their role in reducing greenhouse gas emissions and combating climate change. These incentives, ranging from direct subsidies to tax breaks, are designed to offset the higher upfront costs of EVs compared to traditional internal combustion engine (ICE) vehicles. For instance, Norway, a global leader in EV adoption, offers substantial benefits such as exemption from value-added tax (VAT), import taxes, and registration fees, making EVs more affordable than their ICE counterparts. This approach has propelled Norway to achieve over 80% EV sales in 2022, demonstrating the effectiveness of robust government support.

Subsidies are among the most direct tools governments use to encourage EV purchases. In the United States, the federal government provides a tax credit of up to $7,500 for eligible EV buyers, though this credit phases out once a manufacturer sells 200,000 qualifying vehicles. States like California and New York supplement this with additional rebates, such as California’s Clean Vehicle Rebate Project, which offers up to $7,000 for low-income buyers. Similarly, Germany’s "environmental bonus" provides up to €6,750 for purchasing a new EV, shared equally between the government and automakers. These subsidies not only reduce the purchase price but also signal government commitment to sustainable transportation.

Tax breaks and reduced fees further sweeten the deal for prospective EV buyers. Many countries, including Canada and the UK, offer exemptions or reductions in sales taxes, registration fees, and annual road taxes for EVs. In British Columbia, Canada, EV buyers are exempt from provincial sales tax (PST) up to $3,000, while the UK eliminates vehicle excise duty (VED) for zero-emission cars. Such measures lower the total cost of ownership, making EVs more attractive to cost-conscious consumers. Additionally, some regions provide incentives for installing home charging stations, such as the U.S. federal tax credit of 30% (up to $1,000) for charger installation costs.

Beyond financial incentives, governments are implementing policies to enhance the practicality of EV ownership. For example, many cities offer free parking, access to carpool lanes, and reduced toll rates for EVs. In Paris, EVs are exempt from the city’s congestion charge, while in China, EV owners in Beijing can bypass the city’s strict license plate lottery system. Such perks address non-monetary barriers to adoption, improving the overall EV ownership experience. However, policymakers must ensure these benefits are equitable, as low-income households may still face challenges accessing EVs despite incentives.

While government incentives have proven effective in boosting EV sales, their long-term sustainability and impact require careful consideration. As EV markets mature, subsidies may need to be phased out to avoid over-reliance on public funds. For instance, several countries are transitioning from purchase incentives to investments in charging infrastructure and battery recycling programs. Policymakers must also balance incentives with broader environmental goals, ensuring that EVs are powered by renewable energy to maximize their climate benefits. By strategically designing and evolving these policies, governments can foster a self-sustaining EV market that aligns with global sustainability targets.

Electric Cars and Braking Systems: Debunking Common Myths and Misconceptions

You may want to see also

Explore related products

![]()

Charging Infrastructure: Assessing availability and expansion of EV charging stations worldwide

The global electric vehicle (EV) market is surging, with sales surpassing 10 million units in 2022, a 55% increase from the previous year. However, this rapid growth hinges on a critical factor: the availability and expansion of charging infrastructure. Without a robust network of charging stations, range anxiety persists, stifling widespread EV adoption.

As of 2023, the global charging station count exceeds 2 million, but distribution is uneven. China leads with over 1 million stations, while Europe and North America lag behind. This disparity highlights the need for targeted investment and strategic planning to ensure equitable access to charging, particularly in rural areas and developing nations.

Expanding charging infrastructure requires a multi-pronged approach. Governments play a pivotal role through incentives, subsidies, and streamlined permitting processes. Public-private partnerships are essential, leveraging the expertise and resources of energy companies, automakers, and technology providers. Innovative solutions like wireless charging and battery swapping technologies hold promise, but their large-scale implementation faces technical and economic hurdles.

A key consideration is the type of charging stations. Level 2 chargers, offering 3-20 kW, are suitable for overnight charging at homes and workplaces. DC fast chargers, delivering 50 kW and above, are crucial for long-distance travel, but their high cost and power demands necessitate careful grid integration.

The future of EV charging lies in smart grid integration and renewable energy sources. Vehicle-to-grid (V2G) technology allows EVs to feed power back into the grid during peak demand, transforming them into mobile energy storage units. Pairing charging stations with solar panels or wind turbines reduces reliance on fossil fuels and promotes a sustainable transportation ecosystem.

Ultimately, the success of the EV market depends on a charging infrastructure that is not only widespread but also reliable, accessible, and sustainable. By addressing these challenges through collaboration, innovation, and forward-thinking policies, we can pave the way for a future where electric mobility is the norm, not the exception.

How Electric Cars Work: A Patreon Guide to EV Technology

You may want to see also

Explore related products

![]()

Competitive Landscape: Examining key players, market share, and emerging EV manufacturers

The electric vehicle (EV) market is a battleground where established automakers and agile startups vie for dominance. At the forefront stands Tesla, the undisputed leader with a global market share of approximately 20% in 2023. Tesla’s success stems from its vertical integration, innovative battery technology, and cult-like brand loyalty. However, its position is under threat as traditional automakers like BYD surge ahead, particularly in China, where BYD captured 36% of the domestic EV market in 2023, surpassing Tesla. BYD’s dominance in its home market highlights the importance of localized strategies and government support in shaping competitive advantage.

While Tesla and BYD dominate headlines, legacy automakers are rapidly closing the gap. Volkswagen Group, for instance, invested $86 billion in EV development and aims to sell 50% EVs by 2030. Its ID.4 model has become a bestseller in Europe, showcasing how established players can leverage their manufacturing scale and dealership networks. Similarly, GM and Ford are making strides in the U.S. market with models like the Chevrolet Bolt and F-150 Lightning, respectively. These companies’ ability to repurpose existing infrastructure gives them a cost advantage over pure-play EV manufacturers, though they must overcome brand perception challenges.

Emerging EV manufacturers are disrupting the landscape with niche offerings and innovative business models. Rivian, for example, focuses on premium electric trucks and SUVs, targeting outdoor enthusiasts with features like built-in camp kitchens. Lucid Motors positions itself as a luxury competitor to Tesla, boasting industry-leading range and cutting-edge interior design. Meanwhile, Nio in China offers a unique battery-as-a-service model, reducing upfront costs for consumers. These startups may lack the scale of larger players, but their agility and focus on specific market segments allow them to carve out profitable niches.

Market share dynamics are further complicated by regional variations. In Europe, Stellantis (owner of Peugeot and Fiat) and Hyundai-Kia are strong contenders, benefiting from stringent emissions regulations and consumer incentives. In contrast, the U.S. market remains fragmented, with Tesla leading but facing increasing pressure from domestic and international rivals. China, the world’s largest EV market, is a battleground for both local and global players, with Geely and Xpeng gaining traction alongside BYD. Understanding these regional differences is critical for manufacturers aiming to expand their footprint.

To navigate this competitive landscape, EV manufacturers must prioritize three strategies: differentiation, partnerships, and scalability. Differentiation can come from technology (e.g., faster charging), design, or customer experience. Partnerships with battery suppliers, software developers, or even competitors can accelerate innovation and reduce costs. Scalability, both in production and market reach, will determine long-term viability. As the EV market matures, only those who master these elements will secure a lasting position in this high-stakes race.

Fixing Your Renault Megane's Electric Car Window: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Technological Advancements: Impact of battery tech, range improvements, and autonomous features on EV market

Battery technology stands as the cornerstone of electric vehicle (EV) adoption, and recent advancements are reshaping the market. Modern lithium-ion batteries now boast energy densities exceeding 250 Wh/kg, a 50% increase from a decade ago. This leap translates to longer ranges—some EVs now travel over 400 miles on a single charge, rivaling gasoline vehicles. For instance, Tesla’s Model S Long Range offers 405 miles, while Lucid Air claims up to 520 miles. Such improvements address "range anxiety," a primary barrier to EV adoption, making electric cars more practical for daily use and long-distance travel.

Range improvements aren’t just about battery capacity; they’re also tied to efficiency gains. Advances in motor technology and regenerative braking systems have increased overall vehicle efficiency by 20-30% in the past five years. For example, Hyundai’s Ioniq 6 achieves an EPA-rated 140 MPGe, outperforming many competitors. This efficiency, combined with larger batteries, ensures drivers spend less time charging and more time driving. Practical tip: When shopping for an EV, prioritize models with both high range and efficiency ratings to maximize convenience.

Autonomous features are another technological driver of EV market growth, blending sustainability with cutting-edge innovation. Tesla’s Autopilot and GM’s Super Cruise exemplify Level 2 autonomy, offering hands-free driving on highways. These features not only enhance safety but also position EVs as the platform of choice for future autonomous vehicles. Market data shows that 40% of EV buyers cite advanced driver-assistance systems (ADAS) as a key purchasing factor. However, caution is advised: while these features reduce driver workload, they aren’t fully autonomous, and drivers must remain attentive.

The interplay of battery tech, range, and autonomy is creating a virtuous cycle in the EV market. Improved batteries enable longer ranges, which in turn make EVs more appealing to a broader audience. Simultaneously, autonomous features differentiate EVs from traditional vehicles, attracting tech-savvy consumers. For instance, China’s EV market, the largest globally, saw a 68% year-over-year growth in 2023, driven partly by models like the BYD Han, which combines a 375-mile range with advanced ADAS. This trend underscores how technological advancements are not just enhancing EVs but redefining their market potential.

To capitalize on these advancements, consumers should focus on three key factors: battery size (measured in kWh), range (EPA-rated miles), and autonomy features (e.g., adaptive cruise control, lane-keeping assist). For instance, a 100 kWh battery typically supports ranges above 300 miles, ideal for families or long commutes. Additionally, leasing an EV can be a smart strategy to stay updated with rapid tech improvements without long-term commitment. As battery costs continue to drop—projected to fall below $100/kWh by 2025—EVs will become even more affordable, further accelerating market growth.

Optimal Use of Cooling Fans in Electrical Enclosures: A Guide

You may want to see also

Frequently asked questions

The global electric car market was valued at approximately $287 billion in 2023 and is projected to grow significantly, with estimates reaching over $1 trillion by 2030, driven by increasing environmental concerns and government incentives.

China, Europe, and the United States are the largest markets for electric cars, accounting for over 80% of global sales. China leads with the highest adoption rate, followed by Europe, where stringent emissions regulations boost demand.

Key drivers include declining battery costs, government subsidies and tax incentives, stricter emissions regulations, rising fuel prices, and growing consumer awareness of environmental sustainability.

Challenges include high upfront costs, limited charging infrastructure, range anxiety, long charging times, and concerns over battery production and recycling. Addressing these issues is crucial for wider adoption.