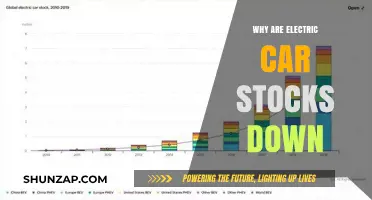

Chinese electric cars are notably absent from the U.S. market due to a combination of regulatory hurdles, trade tensions, and consumer perceptions. Stringent safety and emissions standards set by the National Highway Traffic Safety Administration (NHTSA) and the Environmental Protection Agency (EPA) pose significant challenges for Chinese manufacturers, who must invest heavily to meet these requirements. Additionally, ongoing trade disputes between the U.S. and China, including tariffs and national security concerns, have created economic barriers that discourage Chinese automakers from entering the American market. Furthermore, U.S. consumers often associate Chinese brands with lower quality and reliability, a perception that Chinese companies have yet to overcome. While some Chinese automakers, like BYD, have expressed interest in expanding globally, their presence in the U.S. remains limited, leaving the market dominated by domestic and European electric vehicle brands.

Explore related products

What You'll Learn

- Regulatory Barriers: US safety and emissions standards differ, complicating Chinese EV certification

- Trade Tensions: Tariffs and political disputes hinder Chinese automakers' market entry

- Consumer Perception: US buyers often associate Chinese brands with lower quality or reliability

- Charging Infrastructure: Incompatible charging networks limit practicality for Chinese EVs in the US

- Local Competition: Established US and global EV brands dominate, reducing market opportunities

![]()

Regulatory Barriers: US safety and emissions standards differ, complicating Chinese EV certification

Chinese electric vehicles (EVs) face a significant hurdle in entering the U.S. market due to the stark differences in safety and emissions regulations between the two countries. The United States maintains some of the most stringent automotive standards globally, codified in the Federal Motor Vehicle Safety Standards (FMVSS) and the Environmental Protection Agency’s (EPA) emissions requirements. These regulations are designed to ensure vehicles meet specific crashworthiness, air quality, and performance benchmarks. Chinese EVs, while increasingly competitive in their domestic market and Europe, often struggle to comply with these U.S. standards, which are both technically demanding and costly to meet.

Consider the example of crash safety tests. The FMVSS mandates rigorous assessments, such as the New Car Assessment Program (NCAP), which evaluates frontal, side, and rollover crash performance. Chinese EVs, though improving, have historically lagged in these areas due to differences in testing protocols and engineering priorities. For instance, the IIHS (Insurance Institute for Highway Safety) small overlap front test, a standard U.S. requirement, is less emphasized in China’s C-NCAP program. Retrofitting vehicles to pass these tests requires substantial redesign and investment, often deterring Chinese manufacturers from pursuing U.S. certification.

Emissions standards present another layer of complexity. The EPA’s Tier 3 regulations limit tailpipe emissions and require advanced after-treatment systems, such as selective catalytic reduction (SCR) for NOx reduction. Chinese EVs, while zero-emission at the tailpipe, must still comply with these rules for their battery and manufacturing processes. Additionally, the U.S. Corporate Average Fuel Economy (CAFE) standards impose strict efficiency targets, which Chinese manufacturers may find challenging to meet without significant modifications to their vehicle designs and supply chains.

To navigate these barriers, Chinese automakers must adopt a multi-step approach. First, they should invest in localized engineering teams familiar with U.S. regulatory requirements. Second, partnering with U.S.-based testing facilities can streamline certification processes and ensure compliance. Finally, leveraging modular vehicle platforms that can be adapted to multiple regulatory environments can reduce costs and accelerate market entry. While these steps are resource-intensive, they are essential for Chinese EVs to compete in the U.S. market.

The takeaway is clear: regulatory barriers are not insurmountable but require strategic planning and investment. As Chinese automakers like BYD and Nio expand globally, addressing these differences will be critical to their success in the U.S. market. For consumers, this means the potential for more affordable and innovative EV options—once these regulatory hurdles are cleared.

Choosing the Right Electric Heater Size for Your 3-Car Garage

You may want to see also

Explore related products

![]()

Trade Tensions: Tariffs and political disputes hinder Chinese automakers' market entry

Chinese electric vehicles (EVs) dominate global markets, yet their absence in the U.S. is glaring. This isn't due to lack of innovation or consumer demand, but rather a tangled web of trade tensions, tariffs, and political disputes that effectively block market entry.

Tariffs as Trade Barriers:

The most visible obstacle is the 27.5% tariff imposed on Chinese-made cars entering the U.S. This punitive measure, a relic of the Trump-era trade war, significantly inflates the cost of Chinese EVs, making them uncompetitive against domestically produced and other imported models. For instance, a $30,000 Chinese EV would face an additional $8,250 tariff, pushing its price well above comparable American or European offerings. This price disparity effectively shuts Chinese automakers out of the price-sensitive U.S. market.

Political Rhetoric and National Security Concerns:

Beyond tariffs, political rhetoric and national security concerns further complicate the landscape. Accusations of intellectual property theft, forced technology transfers, and concerns about data privacy related to connected vehicles have fueled a climate of distrust towards Chinese automakers. This has led to legislative proposals aiming to restrict or even ban the sale of Chinese-made EVs in the U.S., citing potential risks to national security.

The Impact on Innovation and Consumer Choice:

The absence of Chinese EVs deprives U.S. consumers of access to cutting-edge technology and competitive pricing. Chinese automakers are leading the way in battery technology, autonomous driving features, and innovative designs. Their exclusion limits consumer choice and stifles competition, potentially slowing down the overall adoption of EVs in the U.S.

A Path Forward: Dialogue and Reciprocity:

Breaking this impasse requires a shift towards constructive dialogue and reciprocity. Negotiating tariff reductions, addressing legitimate security concerns through transparent data practices, and fostering collaboration on technological advancements could pave the way for Chinese EVs to enter the U.S. market. This would not only benefit consumers but also contribute to a more sustainable and competitive automotive industry.

Electric Cars: Transforming the Automotive Industry and Its Future

You may want to see also

Explore related products

![]()

Consumer Perception: US buyers often associate Chinese brands with lower quality or reliability

Chinese brands, particularly in the automotive sector, face an uphill battle in the US market due to deeply ingrained consumer perceptions of inferior quality and reliability. This stereotype, whether justified or not, creates a significant barrier to entry for Chinese electric vehicle (EV) manufacturers. Historical examples, such as the early 2000s influx of low-cost Chinese electronics and appliances that often underperformed, have left a lasting impression on American consumers. Despite advancements in Chinese manufacturing and technology, this legacy of skepticism persists, influencing purchasing decisions and brand trust.

To shift this perception, Chinese EV makers must adopt a multi-faceted strategy. First, they should focus on demonstrating long-term reliability through rigorous third-party testing and transparent data sharing. For instance, showcasing crash test results from the National Highway Traffic Safety Administration (NHTSA) or endurance trials exceeding 100,000 miles could build credibility. Second, partnering with established American brands or dealerships could lend legitimacy and ease consumer concerns about service and support. A practical tip for manufacturers: invest in localized customer service centers to address warranty claims and maintenance promptly, a critical factor for reliability-conscious buyers.

Comparatively, Japanese and Korean automakers faced similar challenges in the US decades ago but overcame them through consistent quality and strategic marketing. Chinese EV brands can learn from this by positioning themselves as innovators, not just cost-effective alternatives. Highlighting cutting-edge features like advanced battery technology or autonomous driving capabilities could reframe the narrative. For example, BYD’s Blade Battery, known for its safety and longevity, could be a selling point if marketed effectively to tech-savvy consumers aged 25–45, who prioritize innovation over brand heritage.

However, caution is necessary. Overpromising or relying solely on price competitiveness can backfire, reinforcing negative stereotypes. Instead, focus on tangible benefits like lower total cost of ownership, including reduced maintenance and energy savings. A persuasive approach could involve offering extended warranties (e.g., 8-year battery coverage) or trial programs to let consumers experience the product risk-free. By addressing reliability concerns head-on and aligning with American consumer values, Chinese EV brands can gradually dismantle the perception barrier and establish a foothold in the US market.

Common Causes of Electrical Issues in Modern Vehicles Explained

You may want to see also

Explore related products

](https://m.media-amazon.com/images/I/317VZcPuzrL._AC_UL320_.jpg)

![]()

Charging Infrastructure: Incompatible charging networks limit practicality for Chinese EVs in the US

Chinese electric vehicles (EVs) face a critical hurdle in the U.S. market: incompatible charging networks. Unlike the standardized CCS (Combined Charging System) prevalent in the U.S., Chinese EVs often rely on GB/T (Guobiao) charging standards, which are incompatible with American infrastructure. This mismatch creates a logistical nightmare for potential buyers, as they would need specialized adapters or entirely new charging stations to power their vehicles. For instance, a BYD Atto 3 owner in the U.S. would struggle to find a public charger compatible with their car’s GB/T port, limiting practicality and convenience.

The incompatibility extends beyond physical connectors to software and communication protocols. U.S. charging networks, such as those operated by ChargePoint or Electrify America, are designed to communicate with CCS-equipped vehicles, ensuring seamless payment and charging processes. Chinese EVs, however, may lack the necessary software integration, leading to errors or failed charging sessions. This technical barrier not only frustrates drivers but also discourages adoption, as reliability is a cornerstone of EV ownership.

To address this issue, Chinese automakers could invest in dual-standard charging ports or partner with U.S. charging networks to upgrade infrastructure. For example, integrating both GB/T and CCS connectors into their vehicles would provide flexibility for U.S. consumers. Alternatively, collaborations with companies like Tesla, which has opened its Supercharger network to non-Tesla EVs, could offer a temporary solution. However, such measures require significant financial and logistical commitment, which many Chinese manufacturers may hesitate to undertake without guaranteed market success.

For consumers considering a Chinese EV, practical steps include researching charging options in their area and investing in adapters where available. Apps like PlugShare or A Better Routeplanner can help locate compatible chargers, though options remain limited. Additionally, home charging installations should prioritize dual-standard compatibility to future-proof the investment. While these workarounds exist, they highlight the broader challenge: until charging networks align, Chinese EVs will remain a niche choice in the U.S., constrained by infrastructure incompatibility.

Are Formula One Race Cars Going Electric? Exploring the Future of F1

You may want to see also

Explore related products

![]()

Local Competition: Established US and global EV brands dominate, reducing market opportunities

The U.S. electric vehicle (EV) market is a fiercely competitive arena, dominated by established brands like Tesla, GM, Ford, and global players such as Volkswagen and Hyundai. These companies have spent decades building brand loyalty, dealer networks, and supply chains, giving them a significant edge over newcomers. For Chinese EV manufacturers, this entrenched competition creates a high barrier to entry. Consumers are already accustomed to the reliability, innovation, and customer service of these established brands, making it difficult for Chinese automakers to carve out a niche without a compelling differentiator.

Consider the example of Tesla, which holds a 50% market share in the U.S. EV sector as of 2023. Tesla’s dominance isn’t just about its vehicles; it’s about its ecosystem—Supercharger networks, over-the-air software updates, and a cult-like following. Chinese brands like BYD or Nio, while innovative in their home market, would need to invest heavily in replicating such infrastructure and brand equity. Similarly, GM and Ford’s legacy in the U.S. auto industry, combined with their aggressive EV strategies (e.g., Ford’s F-150 Lightning), leaves little room for error for new entrants.

To break into this market, Chinese automakers must offer something uniquely valuable. This could mean lower prices, longer ranges, or cutting-edge features. However, even with these advantages, they face regulatory hurdles, tariffs, and consumer skepticism about Chinese brands. For instance, BYD’s Blade Battery technology, which offers superior safety and longevity, could be a selling point, but it’s not enough to offset the lack of brand recognition or local service centers.

A practical tip for Chinese EV manufacturers: Focus on partnerships with U.S. companies or leveraging existing dealer networks to accelerate market penetration. For example, collaborating with a U.S. automaker to co-develop vehicles or using their distribution channels could mitigate some of the challenges. Additionally, targeting niche segments, such as affordable EVs for urban commuters, could provide a foothold before expanding into broader markets.

In conclusion, the dominance of established U.S. and global EV brands creates a crowded and competitive landscape that limits opportunities for Chinese automakers. Success in this market requires more than just innovative products—it demands strategic partnerships, localized infrastructure, and a deep understanding of American consumer preferences. Without these elements, Chinese EVs risk being overshadowed by the giants already ruling the road.

Why Electric Cars Struggle with Short Range: Key Factors Explained

You may want to see also

Frequently asked questions

Chinese electric cars face significant regulatory and trade barriers in the U.S., including stringent safety and emissions standards, as well as tariffs imposed under Section 301 of the Trade Act of 1974, which increase their cost and reduce competitiveness.

Many Chinese manufacturers, such as BYD and Nio, have expressed interest in entering the U.S. market but face challenges like consumer skepticism, political resistance, and the need to establish local infrastructure, such as charging networks and dealerships.

Yes, there are concerns about potential cybersecurity risks and data privacy issues related to Chinese electric vehicles, as U.S. lawmakers worry about data collection and the possibility of foreign government access to sensitive information, which has led to increased scrutiny and restrictions.