An electric company would likely use a process costing system due to the nature of its operations, which involve the continuous and mass production of electricity. Unlike job costing, which is suitable for custom or unique projects, process costing is ideal for industries where the output is homogeneous and produced in large quantities. In the case of an electric company, the generation of electricity involves multiple stages—such as fuel processing, power generation, and distribution—each contributing to the final product. Process costing allows the company to allocate costs evenly across these stages, track expenses for each department or process, and determine the average cost per unit of electricity produced. This system ensures accurate financial reporting, cost control, and efficient management of resources, making it a practical choice for the electric utility industry.

Explore related products

$104.11 $170

What You'll Learn

- Process Costing Basics: Understanding the fundamentals of process costing in manufacturing and service industries

- Electricity Production Flow: How electricity generation aligns with continuous, mass production processes

- Cost Allocation Methods: Tracking and allocating costs across multiple production stages efficiently

- Uniformity in Output: Why electric companies benefit from standardized, consistent output in process costing

- Cost Control Advantages: Using process costing to monitor and reduce production costs effectively

![]()

Process Costing Basics: Understanding the fundamentals of process costing in manufacturing and service industries

Process costing is a method of cost accounting used primarily in manufacturing and service industries where the production process is continuous and homogeneous. It is particularly useful for companies that produce large quantities of identical or similar products, such as chemicals, food, oil, and yes, even electricity. The core principle of process costing is to accumulate and allocate costs across different stages or departments of production, rather than tracking costs for individual units. This approach is essential for industries where it is impractical or impossible to trace costs to specific items due to the nature of the production process. For an electric company, process costing can be highly relevant, especially in power generation plants where raw materials (like coal, natural gas, or water) are transformed into electricity through a series of continuous processes.

In the context of an electric company, the process costing system would track costs at each stage of electricity generation, such as fuel consumption, labor, maintenance, and overhead expenses. For example, a coal-fired power plant would allocate costs to stages like coal handling, combustion, steam generation, and turbine operation. Each department or process accumulates costs, which are then averaged out over the total units produced (in this case, kilowatt-hours of electricity). This method ensures that the cost per unit of electricity is accurately determined, allowing the company to price its product competitively and manage costs effectively. Process costing also helps in identifying inefficiencies or bottlenecks in the production process, enabling management to make informed decisions to improve productivity and reduce waste.

One of the key advantages of process costing is its ability to handle joint products and by-products, which are common in industries like electricity generation. For instance, a power plant might produce electricity as its main product but also generate steam as a by-product that can be sold or used internally. Process costing allows for the allocation of costs between the main product and by-products based on their relative values or quantities. This ensures that the cost of each output is accurately reflected, providing a clearer picture of profitability for each product stream. In the case of an electric company, this could involve separating the costs of electricity generation from the costs associated with steam production or other secondary outputs.

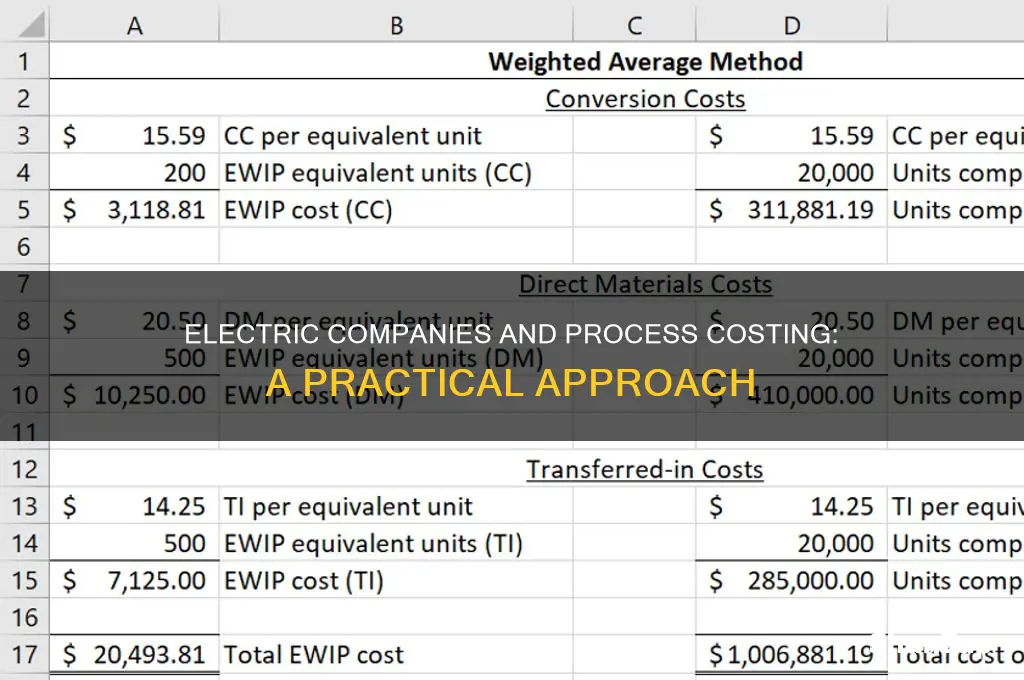

Implementing a process costing system requires careful planning and organization. Companies must define their production processes, identify cost centers, and establish a method for measuring output. In the electricity sector, output is typically measured in kilowatt-hours, and costs are allocated based on the volume of electricity produced at each stage. Additionally, process costing relies on equivalent units of production, which account for partially completed units in the production pipeline. For example, if a power plant has partially processed fuel or partially generated electricity, these units are converted into equivalent completed units to ensure accurate cost allocation. This approach ensures that costs are not overstated or understated, providing a reliable basis for financial reporting and decision-making.

While process costing is highly effective for industries with continuous and mass production, it may not be suitable for every aspect of an electric company’s operations. For instance, maintenance or administrative activities that are not directly tied to the production process might be better managed using job costing or other cost accounting methods. However, for the core function of electricity generation, process costing remains the most appropriate and efficient system. By understanding and applying the fundamentals of process costing, electric companies can streamline their cost management, improve operational efficiency, and maintain a competitive edge in the energy market.

Electric Vehicles: Why Hybrid Series Are Not an Option

You may want to see also

Explore related products

![]()

Electricity Production Flow: How electricity generation aligns with continuous, mass production processes

Electricity generation is inherently aligned with continuous, mass production processes due to its nature as a commodity that must be produced and delivered in large, uninterrupted quantities. Unlike discrete manufacturing, where individual units are produced and tracked, electricity is generated in a continuous flow, making it a prime candidate for process costing systems. Power plants, whether fueled by coal, natural gas, nuclear reactions, or renewable sources like wind and solar, operate 24/7 to meet the constant demand for electricity. This continuous operation mirrors mass production principles, where raw materials (e.g., fuel, water, or sunlight) are transformed into a homogeneous output (electricity) through a series of standardized processes. The flow of electricity production is linear and consistent, with each stage—from fuel processing to power generation and transmission—contributing incrementally to the final product.

The alignment of electricity generation with continuous production processes is further evident in the economies of scale achieved through large-scale operations. Power plants are designed to maximize output efficiency, producing electricity in bulk to serve thousands or even millions of consumers. This mass production approach reduces the cost per unit of electricity generated, a key advantage of process costing systems. For instance, coal-fired plants burn tons of coal hourly to produce steam that drives turbines, while nuclear plants sustain continuous fission reactions to generate heat. These processes are repetitive, standardized, and optimized for high-volume output, ensuring a steady supply of electricity to the grid. The uniformity of the product—electricity—also simplifies cost allocation, as there is no need to differentiate between individual units.

Another critical aspect of electricity production that aligns with process costing is the cumulative nature of costs incurred throughout the production flow. Costs are accumulated at each stage of the process, from fuel procurement and plant maintenance to labor and transmission infrastructure. These costs are then averaged over the total units of electricity produced, a hallmark of process costing. For example, the cost of coal consumed in a power plant is allocated based on the megawatt-hours generated, not on individual units of electricity. This method ensures that costs are distributed equitably across the continuous output, reflecting the true expense of production. Similarly, overhead costs like equipment depreciation and operational expenses are spread across the entire production volume, aligning with the principles of mass production.

The continuous flow of electricity production also necessitates real-time monitoring and cost control, which is facilitated by process costing systems. Power companies must track costs at each stage of production to ensure efficiency and profitability. For instance, fluctuations in fuel prices or unexpected maintenance can impact production costs, requiring adjustments to maintain financial stability. Process costing allows electric companies to analyze costs at each process stage, identify inefficiencies, and optimize operations. This granular cost tracking is essential in an industry where production is uninterrupted and demand is constant, ensuring that electricity remains affordable and accessible to consumers.

Finally, the integration of renewable energy sources into electricity production further underscores the relevance of process costing systems. Solar and wind farms, for example, generate electricity continuously when conditions are favorable, contributing to the overall production flow. While the input (sunlight or wind) is variable, the output is treated as part of the mass production process, with costs allocated based on the total energy generated. This approach ensures that renewable energy is seamlessly integrated into the grid, maintaining the continuity and efficiency of electricity production. In essence, the electricity production flow exemplifies the principles of continuous, mass production processes, making process costing systems an ideal fit for electric companies.

Electric Vehicles: Free from Toll Charges?

You may want to see also

Explore related products

![]()

Cost Allocation Methods: Tracking and allocating costs across multiple production stages efficiently

Electric companies often operate in a complex, multi-stage production environment, where raw materials (such as coal, natural gas, or renewable resources) are transformed through various processes to generate electricity. Given this structure, a process costing system is highly suitable for tracking and allocating costs efficiently across production stages. Process costing aggregates costs by department or process, making it ideal for industries with continuous, mass production, like electricity generation. This system ensures that costs are systematically assigned to each stage—extraction, processing, generation, transmission, and distribution—providing a clear picture of where resources are consumed.

One of the primary cost allocation methods used in process costing is the step-down allocation approach. In this method, costs from service departments (e.g., maintenance or administration) are allocated to production departments in a sequential manner, based on the usage of services. For an electric company, this might involve allocating maintenance costs to the generation stage before distributing them to transmission and distribution stages. This method ensures that costs are traced in the order of production flow, enhancing accuracy and transparency.

Another effective method is activity-based costing (ABC), which allocates costs based on specific activities that drive resource consumption. For instance, an electric company might identify activities like fuel processing, turbine operation, or grid maintenance as cost drivers. By linking costs to these activities, the company can pinpoint inefficiencies and optimize resource allocation across stages. ABC is particularly useful for identifying hidden costs in complex processes, such as those involved in renewable energy production.

Equivalent units of production is another critical concept in process costing for electric companies. Since electricity is produced continuously, it’s essential to determine the cost of partially completed units (e.g., electricity in the transmission stage). This method calculates costs by considering the percentage of completion at each stage, ensuring that costs are allocated proportionally. For example, if 80% of the electricity has completed the generation stage, 80% of the associated costs are allocated accordingly.

Finally, standard costing can be employed to benchmark and control costs across production stages. By setting standard costs for materials, labor, and overhead, an electric company can compare actual costs to expected costs, identifying variances early. This method is particularly useful in stabilizing cost allocation, especially in volatile markets like energy, where input prices fluctuate frequently. Standard costing also aids in budgeting and forecasting, ensuring financial stability across multiple production stages.

In conclusion, electric companies can leverage process costing systems and various cost allocation methods to efficiently track and allocate costs across their multi-stage production processes. Whether through step-down allocation, activity-based costing, equivalent units of production, or standard costing, these methods provide the tools needed to maintain financial control, optimize resource use, and enhance overall operational efficiency in the energy sector.

Electric Blankets in Hospitals: Safety Concerns and Alternatives Explained

You may want to see also

Explore related products

![]()

Uniformity in Output: Why electric companies benefit from standardized, consistent output in process costing

Electric companies often adopt process costing systems due to the inherent nature of their operations, which involve continuous and mass production of electricity. One of the key advantages of this system is the emphasis on uniformity in output, which aligns perfectly with the requirements of the electric utility sector. In process costing, products are standardized, and costs are accumulated over departments or processes rather than individual units. This approach is particularly beneficial for electric companies because electricity generation and distribution inherently rely on consistent, standardized processes to ensure a stable supply of power to consumers. Uniformity in output ensures that the electricity produced meets regulatory standards and customer expectations, regardless of when or where it is generated.

The standardized nature of electricity production allows electric companies to streamline their costing processes. Since electricity is a homogeneous product, process costing enables companies to allocate costs evenly across the entire output. For instance, whether the electricity is generated through coal, natural gas, or renewable sources, the costing system treats the output uniformly, simplifying financial tracking and reporting. This uniformity reduces the complexity of cost allocation, making it easier to manage expenses related to fuel, labor, maintenance, and other operational costs. As a result, electric companies can maintain financial efficiency and transparency, which is crucial for regulatory compliance and stakeholder trust.

Another significant benefit of uniformity in output is the ability to forecast and manage costs more effectively. Electric companies operate in a highly regulated environment where pricing is often controlled by external bodies. By maintaining consistent output standards, companies can predict their production costs with greater accuracy, enabling better budgeting and financial planning. This predictability is essential for long-term investments in infrastructure, such as power plants or grid upgrades, as it ensures that resources are allocated efficiently. Additionally, standardized output facilitates benchmarking, allowing companies to compare their performance against industry standards and identify areas for improvement.

Uniformity in output also enhances operational efficiency by minimizing variability in production processes. Electric companies rely on continuous operations, and any deviations in output quality or quantity can lead to disruptions in supply. By standardizing processes, companies can reduce the risk of errors, downtime, and waste, ensuring a reliable and consistent supply of electricity. This reliability is critical for meeting customer demand and avoiding penalties or reputational damage due to power outages or fluctuations. Furthermore, standardized processes enable easier training of personnel, as employees can follow established protocols, reducing the learning curve and improving overall productivity.

Finally, the focus on uniformity in output supports sustainability and innovation in the electric utility sector. As companies transition to renewable energy sources, standardized processes ensure that new technologies can be integrated seamlessly into existing operations. For example, whether generating electricity from solar panels or wind turbines, the process costing system treats the output uniformly, simplifying cost management and performance evaluation. This uniformity encourages investment in green technologies by providing a clear framework for assessing their financial and operational impact. In this way, electric companies can align their production processes with environmental goals while maintaining economic viability.

In conclusion, uniformity in output is a cornerstone of process costing systems, and electric companies derive significant benefits from this approach. It ensures consistent product quality, simplifies cost management, enhances operational efficiency, and supports long-term sustainability. By standardizing their output, electric companies can navigate the complexities of their industry more effectively, delivering reliable and affordable electricity to consumers while maintaining financial health and regulatory compliance.

Are Electric Wheelchairs Classified as Electric Vehicles?

You may want to see also

Explore related products

![]()

Cost Control Advantages: Using process costing to monitor and reduce production costs effectively

Electric companies, particularly those involved in the production of electricity through processes like power generation, can significantly benefit from implementing a process costing system. This system is particularly well-suited for industries where the production process is continuous and involves the transformation of raw materials into finished products in a sequential manner. In the context of an electric company, process costing can be applied to monitor and control costs associated with generating electricity, ensuring efficiency and cost-effectiveness.

One of the primary cost control advantages of using process costing is the ability to track costs at each stage of production. For an electric company, this means monitoring the expenses incurred in various phases of electricity generation, such as fuel consumption, labor, maintenance, and overhead costs. By breaking down the production process into distinct stages, companies can identify cost drivers and allocate resources more efficiently. For instance, if a particular stage, like coal handling or turbine maintenance, is found to be more costly, management can focus on optimizing that specific area, thereby reducing overall production costs.

Another advantage is the facilitation of cost comparison and benchmarking. Process costing allows electric companies to compare the costs of different production runs or time periods, enabling them to identify trends and anomalies. This comparative analysis can highlight inefficiencies and provide insights into best practices. For example, by comparing the cost of electricity generation during peak and off-peak hours, companies can adjust their operations to minimize costs during high-demand periods. Additionally, benchmarking against industry standards or other power plants can reveal areas for improvement and cost reduction.

Real-time cost monitoring is a critical benefit of process costing, enabling electric companies to make informed decisions promptly. With a process costing system, companies can generate regular reports on production costs, allowing management to quickly identify deviations from the budget. This real-time visibility ensures that any cost overruns are addressed immediately, preventing minor issues from escalating into major financial problems. For instance, if the cost of natural gas suddenly spikes, the system can alert managers, who can then decide to switch to a more cost-effective fuel source or adjust production schedules accordingly.

Furthermore, process costing supports cost reduction through standardization and process improvement. By analyzing the costs associated with each process step, electric companies can standardize procedures to eliminate waste and inefficiency. This might involve implementing lean manufacturing principles or investing in technology upgrades to streamline operations. For example, automating certain stages of power generation can reduce labor costs and minimize human error, leading to significant long-term savings. The data provided by process costing can also justify capital expenditures by demonstrating the potential return on investment in terms of reduced production costs.

In summary, adopting a process costing system offers electric companies a robust framework for monitoring and reducing production costs effectively. It provides detailed insights into cost structures, enables comparative analysis, facilitates real-time decision-making, and promotes continuous process improvement. By leveraging these advantages, electric companies can enhance their cost control strategies, ultimately improving profitability and competitiveness in the energy market.

Chevy Volt: Plug-In Hybrid Electric Vehicles Explored

You may want to see also

Frequently asked questions

Yes, an electric company would likely use a process costing system, especially for generating electricity, as it involves continuous, mass production processes where costs are accumulated over time and allocated to units produced.

Process costing is suitable because electricity production involves homogeneous outputs (e.g., kilowatt-hours) produced in large quantities through sequential stages (e.g., generation, transmission, distribution), making it easier to track and allocate costs per unit.

Challenges include accurately allocating costs across multiple stages, accounting for varying production volumes, and handling fluctuations in input costs (e.g., fuel prices), which require careful monitoring and adjustments in the costing system.