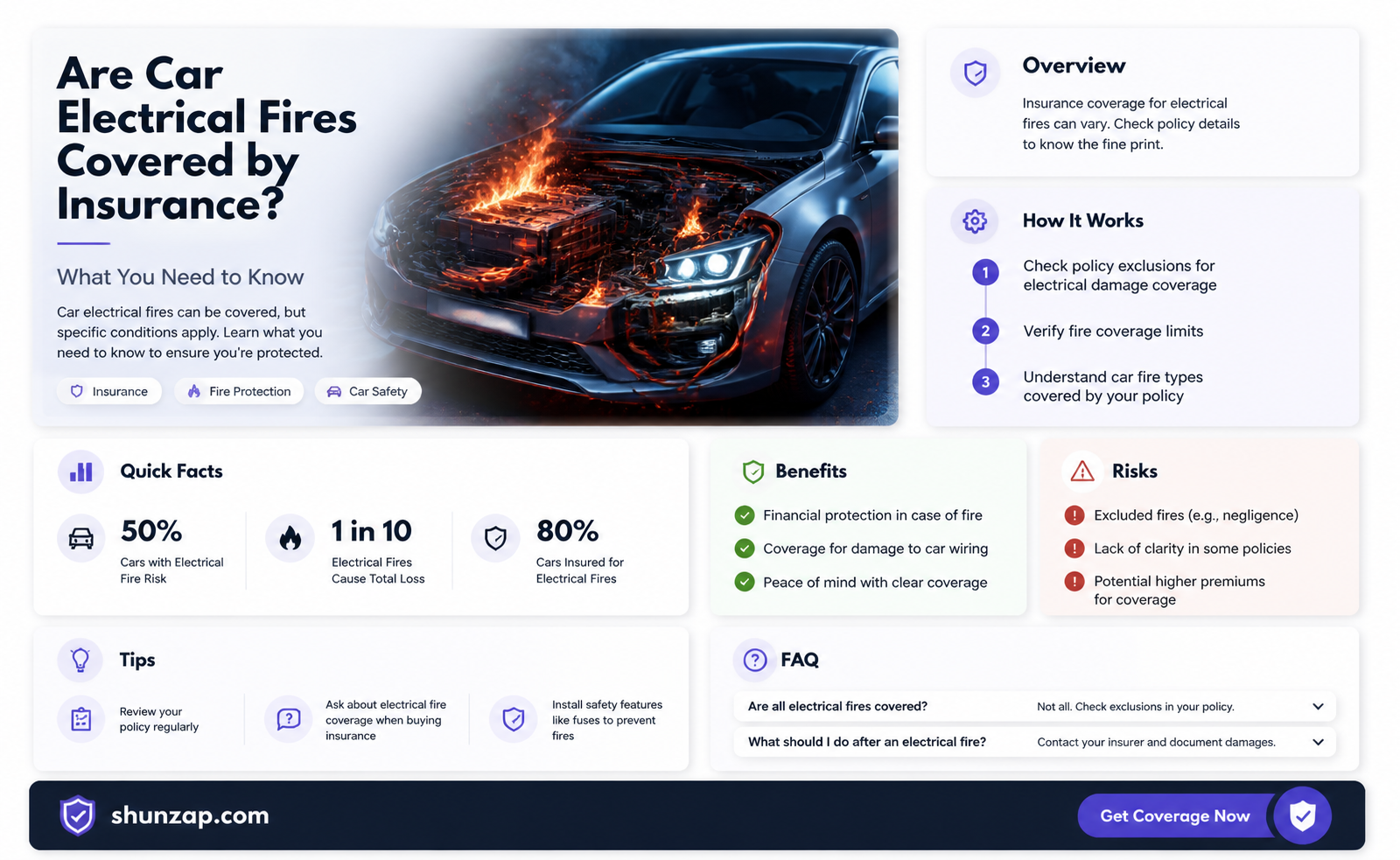

Car electrical fires are a growing concern for vehicle owners, as modern vehicles increasingly rely on complex electrical systems that can malfunction and lead to fires. When such an incident occurs, one of the first questions owners ask is whether their insurance policy covers the damage. Generally, comprehensive auto insurance policies often include coverage for fire damage, including electrical fires, as long as the fire was not caused by negligence or intentional actions. However, the specifics can vary widely depending on the policy, the insurance provider, and the circumstances of the fire. It’s essential for car owners to review their insurance policies carefully and consult with their insurer to understand their coverage limits and any potential exclusions related to electrical fires.

| Characteristics | Values |

|---|---|

| Coverage Type | Comprehensive insurance typically covers car electrical fires. |

| Cause of Fire | Covered if caused by electrical system failure, short circuits, or faults. |

| Exclusions | Not covered if fire results from negligence, lack of maintenance, or intentional acts. |

| Policy Deductible | Applies; amount varies by policy and insurer. |

| Vehicle Age Impact | Older vehicles may have limited coverage or higher premiums. |

| Modification Impact | Aftermarket electrical modifications may affect coverage. |

| Total Loss Coverage | Pays up to the vehicle's actual cash value (ACV) if totaled. |

| Rental Car Coverage | May include rental car reimbursement during repairs (if added to policy). |

| Liability Coverage | Does not apply; electrical fires are not liability claims. |

| Insurance Company Discretion | Coverage depends on policy terms and insurer's assessment of the claim. |

| Documentation Required | Proof of fire cause, repair estimates, and vehicle ownership. |

| Preventive Measures | Regular maintenance can reduce risk but does not guarantee coverage. |

| State Regulations | Coverage may vary slightly based on local insurance laws. |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Comprehensive Coverage Details

When considering whether car electrical fires are covered by insurance, it's essential to delve into the specifics of Comprehensive Coverage Details. Comprehensive car insurance is designed to protect against a wide range of non-collision-related incidents, including events like theft, vandalism, natural disasters, and yes, electrical fires. This coverage typically extends beyond the basic liability and collision policies, offering a safety net for vehicle owners against unforeseen damages that are not caused by accidents. For electrical fires, comprehensive coverage is often the policy component that would come into play, as these incidents are generally classified under "other than collision" claims.

One of the key aspects of Comprehensive Coverage Details is understanding what constitutes an electrical fire. These fires can result from faulty wiring, malfunctioning components, or even issues with the vehicle's battery. Insurance providers usually cover such damages if the fire is deemed accidental and not a result of negligence or lack of maintenance. For instance, if an electrical fire occurs due to a manufacturing defect, comprehensive coverage would likely apply. However, if the fire is caused by ignored warning signs or failure to address known electrical issues, the claim might be denied.

Another important factor in Comprehensive Coverage Details is the policy's deductible. When filing a claim for an electrical fire, the policyholder is typically responsible for paying the deductible before the insurance company covers the remaining repair or replacement costs. Deductibles vary widely depending on the policy, so it’s crucial to review your coverage limits and deductible amount to understand your financial responsibility in such scenarios. Some policies may also offer additional benefits, such as rental car reimbursement while your vehicle is being repaired, which can be particularly useful in the aftermath of a fire.

It’s also worth noting that Comprehensive Coverage Details may include exclusions or limitations. Certain high-risk vehicles or custom modifications might not be fully covered, especially if they increase the likelihood of electrical issues. Additionally, some insurers may require proof of regular maintenance to validate a claim. For example, if a fire is traced back to a neglected battery or ignored electrical warnings, the insurer might argue that the damage was preventable and deny the claim. Therefore, maintaining detailed records of vehicle upkeep can be invaluable when dealing with insurance claims related to electrical fires.

Lastly, when evaluating Comprehensive Coverage Details, it’s advisable to consult directly with your insurance provider to clarify any ambiguities. Policies can differ significantly between companies, and understanding the nuances of your specific coverage ensures you’re adequately protected. Some insurers may offer optional add-ons or endorsements that provide additional protection for electrical systems or high-tech components, which could be beneficial for modern vehicles with advanced electronics. By thoroughly reviewing your policy and discussing potential risks with your insurer, you can ensure that you’re prepared for the financial implications of an electrical fire.

Firefighter Preparedness for Electric Vehicle Fires: Are They Ready?

You may want to see also

Explore related products

![]()

Exclusions in Policies

When considering whether car electrical fires are covered by insurance, it's crucial to understand the exclusions in policies that may apply. Most standard auto insurance policies provide coverage under the comprehensive insurance section, which typically includes protection against non-collision incidents like fire. However, not all fires are treated equally, and certain conditions or circumstances can lead to coverage being denied. For instance, if the fire is determined to have resulted from negligence, such as failure to maintain the vehicle’s electrical system or ignoring known issues, the insurer may exclude the claim. This is because insurers expect policyholders to take reasonable steps to prevent foreseeable damage.

Another common exclusion in policies relates to wear and tear or mechanical breakdowns. Comprehensive insurance is generally designed to cover sudden and accidental events, not gradual deterioration of the vehicle’s components. If an electrical fire is traced back to a worn-out wiring system or a failing alternator that the owner neglected to repair, the insurer may deny the claim. This exclusion underscores the importance of regular vehicle maintenance to avoid coverage gaps. Policyholders should review their policies to understand whether their insurer specifically excludes damage caused by mechanical failures.

Intentional acts are also a significant exclusion in auto insurance policies. If an investigation reveals that the electrical fire was deliberately caused by the policyholder or someone acting on their behalf, the claim will almost certainly be denied. Insurance is intended to protect against accidental losses, not fraudulent or malicious behavior. Additionally, if the vehicle was being used for illegal activities at the time of the fire, coverage may be voided, as insurers typically exclude losses arising from unlawful actions.

Some policies may exclude coverage for electrical fires if the vehicle was modified without disclosure. Aftermarket electrical systems or modifications that increase the risk of fire, such as high-performance audio systems or custom lighting, may not be covered unless explicitly declared to the insurer. Failure to inform the insurer about such modifications can result in a denied claim, as it violates the principle of utmost good faith in insurance contracts. Policyholders should always update their insurer about any changes to their vehicle to ensure continuous coverage.

Lastly, lapsed policies or insufficient coverage limits can lead to exclusions. If the policy was not active at the time of the electrical fire, the insurer will not provide coverage. Similarly, if the policy’s coverage limits are too low to account for the full extent of the damage, the policyholder may be left to cover the remaining costs out of pocket. It’s essential to maintain an active policy and ensure that coverage limits are adequate to protect against potential losses, including those caused by electrical fires. Understanding these exclusions in policies is key to avoiding unexpected financial burdens.

Ford's Electric Vehicle Future: What's the Plan?

You may want to see also

Explore related products

![]()

Claim Process Steps

When dealing with a car electrical fire and navigating the insurance claim process, it's essential to understand the steps involved to ensure a smooth and successful claim. The first step is to report the incident to your insurance company as soon as possible. Most insurance policies require prompt notification of any accidents or damages. Contact your insurance agent or the company's claims department via phone, email, or their online portal. Provide them with your policy number, vehicle details, and a brief description of the electrical fire incident. Timely reporting is crucial, as delays might complicate the claims process and could potentially lead to denial of coverage.

Document the damage extensively to support your claim. Take clear photographs or videos of the vehicle, focusing on the areas affected by the electrical fire. Capture multiple angles and close-ups of any visible damage, including burnt wires, melted components, or charred interiors. If possible, take pictures of the entire vehicle to provide a comprehensive view of the damage. Additionally, make notes about the incident, including the date, time, and any relevant circumstances leading up to the fire. Gather any available evidence, such as witness statements or police reports, if the fire resulted in an accident or required emergency services.

The next step is to review your insurance policy to understand the coverage details. Comprehensive car insurance policies typically cover damages caused by fire, including electrical fires. However, it's essential to verify the specifics of your policy. Look for sections related to 'covered perils' or 'comprehensive coverage' to confirm that fire damage is included. Pay attention to any exclusions or limitations, such as negligence or lack of maintenance, which might impact your claim. Understanding your policy will help you set realistic expectations and prepare the necessary documentation.

File a formal claim with your insurance provider, providing all the gathered information and evidence. This usually involves submitting a claim form, which can often be done online or through a mobile app. Include the photos, videos, and any other supporting documents. Provide a detailed description of the electrical fire, the damage sustained, and any repairs or replacements needed. Be thorough and accurate in your claim submission to avoid delays or requests for additional information. After filing, you will likely receive a claim number, which you should use for all future communications regarding this incident.

Once the claim is submitted, an insurance adjuster will be assigned to assess the damage and determine the coverage. They may request additional information or schedule an inspection of the vehicle. Cooperate with the adjuster and provide any further details they require. The adjuster will evaluate the cause of the electrical fire and the extent of the damage to decide on the claim settlement. This process might involve negotiating repair costs with mechanics or assessing the vehicle's total loss value if the damage is severe. Stay in communication with your insurance company during this period and promptly respond to any inquiries.

Finally, understand the claim settlement process and your rights. If your claim is approved, the insurance company will provide compensation based on the policy terms. This could involve direct payment to a repair shop or reimbursement for repairs already completed. In total loss cases, they will offer a settlement based on the vehicle's market value. Review the settlement offer carefully and ask for clarification if needed. If you disagree with the decision, you have the right to dispute it and provide additional evidence to support your case. Knowing your rights and staying informed throughout the process is essential to ensuring a fair outcome.

The Next Big Electric Vehicle Launch in the US

You may want to see also

Explore related products

![]()

Liability vs. Full Coverage

When considering whether car electrical fires are covered by insurance, it's essential to understand the difference between liability insurance and full coverage policies. Liability insurance is the minimum coverage required by most states and typically covers damages or injuries you cause to others in an accident. However, it does not cover damages to your own vehicle, including those caused by electrical fires. If an electrical fire in your car results in damage to someone else’s property or injures another person, liability insurance would cover their losses, but it leaves you financially responsible for repairing or replacing your own vehicle.

In contrast, full coverage insurance combines liability insurance with collision and comprehensive coverage. Comprehensive coverage is particularly relevant to car electrical fires, as it protects against non-collision-related incidents, such as fire, theft, vandalism, and natural disasters. If an electrical fire damages your vehicle, comprehensive coverage would typically pay for the repairs or the vehicle’s value if it’s totaled, minus your deductible. This makes full coverage a more robust option for protecting your vehicle from unforeseen events like electrical fires.

The key distinction between liability and full coverage lies in their scope of protection. Liability insurance is designed to protect others, while full coverage protects both you and others. For car electrical fires, full coverage is the only option that ensures your vehicle is covered, whereas liability insurance would leave you without financial assistance for your own repairs. This is why full coverage is often recommended for vehicle owners who want comprehensive protection against a wide range of risks.

Another factor to consider is the cause of the electrical fire. If the fire is determined to be the result of a manufacturing defect or a covered peril under your policy, comprehensive coverage within a full coverage policy would likely apply. However, if the fire is due to negligence or lack of maintenance, the insurance company might deny the claim. Liability insurance, on the other hand, would not cover your vehicle regardless of the cause, further emphasizing the limitations of this type of policy.

Ultimately, when deciding between liability and full coverage, think about your vehicle’s value and your financial situation. If your car is newer or financed, full coverage is often a wiser choice because it provides broader protection, including for electrical fires. Liability insurance, while more affordable, leaves significant gaps in coverage that could result in substantial out-of-pocket expenses if your vehicle is damaged by fire or other non-collision events. Understanding these differences ensures you can make an informed decision about the level of protection you need for your vehicle.

Battery Costs: A Major Factor in Electric Vehicle Pricing

You may want to see also

Explore related products

![]()

Preventive Measures Impact

Car electrical fires can be devastating, but understanding the role of preventive measures can significantly impact whether insurance covers such incidents. Insurance policies often assess the cause of the fire to determine liability. If the fire results from negligence, such as ignoring warning signs or failing to maintain the vehicle, coverage may be denied. Conversely, if the fire occurs despite the owner taking reasonable preventive steps, insurance is more likely to provide compensation. This highlights the importance of proactive measures in not only preventing fires but also ensuring financial protection.

Regular vehicle maintenance is a critical preventive measure that directly impacts insurance coverage. Routine checks of the electrical system, including wiring, fuses, and battery connections, can identify potential hazards before they escalate. Insurance companies often view consistent maintenance as evidence of responsible ownership, which can strengthen a claim in the event of a fire. Keeping detailed records of maintenance and repairs further supports the case that the owner took reasonable steps to prevent the incident, potentially influencing the insurer's decision in their favor.

Installing safety devices, such as circuit breakers or fire extinguishers, is another preventive measure that can impact insurance outcomes. These devices reduce the risk of electrical fires and minimize damage if a fire occurs. Some insurance providers offer discounts or favorable terms for vehicles equipped with such safety features, recognizing their role in mitigating risks. By investing in these tools, car owners not only enhance safety but also improve their chances of receiving insurance coverage if an electrical fire happens.

Driver education and awareness play a significant role in preventive measures and their impact on insurance claims. Understanding warning signs like burning smells, flickering lights, or unusual sounds can prompt timely action to address electrical issues. Insurance companies may consider the owner's response to these signs when evaluating a claim. Quick action to diagnose and fix problems demonstrates responsibility, which can positively influence the insurer's assessment of the situation.

Finally, choosing comprehensive insurance coverage is a preventive measure in itself, as it typically includes protection against non-collision incidents like electrical fires. While this doesn’t prevent fires, it ensures financial security if one occurs. Pairing comprehensive coverage with proactive maintenance and safety measures creates a robust defense against both the physical and financial consequences of car electrical fires. This dual approach maximizes the likelihood of insurance coverage while minimizing the risk of fire-related incidents.

Lexus Electrification: All-Electric Vehicles on the Horizon?

You may want to see also

Frequently asked questions

Yes, comprehensive car insurance typically covers car electrical fires, as they are considered a non-collision-related incident.

No, liability-only insurance does not cover damage to your own vehicle, including electrical fires. Comprehensive coverage is needed for such incidents.

Yes, filing a claim for a car electrical fire may increase your insurance premiums, as it is considered a risk factor by insurers.

Coverage may be denied if the electrical fire is determined to be the result of negligence or poor maintenance, as insurers typically expect policyholders to maintain their vehicles properly.