The electric car tax credit is a financial incentive offered by governments to encourage the adoption of electric vehicles (EVs) and reduce greenhouse gas emissions. This credit, typically applied at the federal or state level, allows eligible buyers to deduct a portion of their EV purchase cost from their taxes, effectively lowering the overall price of the vehicle. To qualify, the car must meet specific criteria, such as battery capacity and manufacturer requirements, and the credit amount can vary based on factors like the vehicle's battery size and the taxpayer's income. Understanding how this tax credit works is essential for potential EV buyers looking to maximize their savings while contributing to a more sustainable future.

Explore related products

What You'll Learn

- Eligibility Requirements: Income limits, vehicle price caps, and manufacturer restrictions for claiming the tax credit

- Credit Amount: Maximum credit value, phase-out rules, and how it’s applied to taxes owed

- Qualifying Vehicles: Criteria for EVs, including battery size, assembly location, and model eligibility

- Claiming Process: How to file for the credit on tax returns and required documentation

- Recent Changes: Updates to tax credit laws, including Inflation Reduction Act modifications

![]()

Eligibility Requirements: Income limits, vehicle price caps, and manufacturer restrictions for claiming the tax credit

To claim the electric vehicle (EV) tax credit, understanding the eligibility requirements is crucial. These requirements are designed to ensure that the credit benefits specific groups and promotes the adoption of electric vehicles within certain parameters. The eligibility criteria primarily revolve around income limits, vehicle price caps, and manufacturer restrictions.

Income Limits: The electric vehicle tax credit is subject to income restrictions to ensure it benefits middle and lower-income households. As of the latest guidelines, individuals with a modified adjusted gross income (MAGI) exceeding certain thresholds may not qualify for the full credit. For example, single filers with a MAGI above $150,000, heads of household above $225,000, and married couples filing jointly above $300,000 may face a phase-out of the credit. This means the credit amount decreases as income rises above these limits, and it phases out completely once income exceeds $200,000 for single filers, $300,000 for heads of household, and $400,000 for married couples filing jointly.

Vehicle Price Caps: Another critical eligibility factor is the vehicle's price. The tax credit applies only to new electric vehicles, and there is a cap on the vehicle's manufacturer suggested retail price (MSRP). Vehicles with an MSRP above $80,000 for vans, SUVs, and pickups, and $55,000 for other vehicles, are ineligible for the credit. This ensures that the credit is targeted towards more affordable electric vehicles, encouraging broader adoption without subsidizing luxury models.

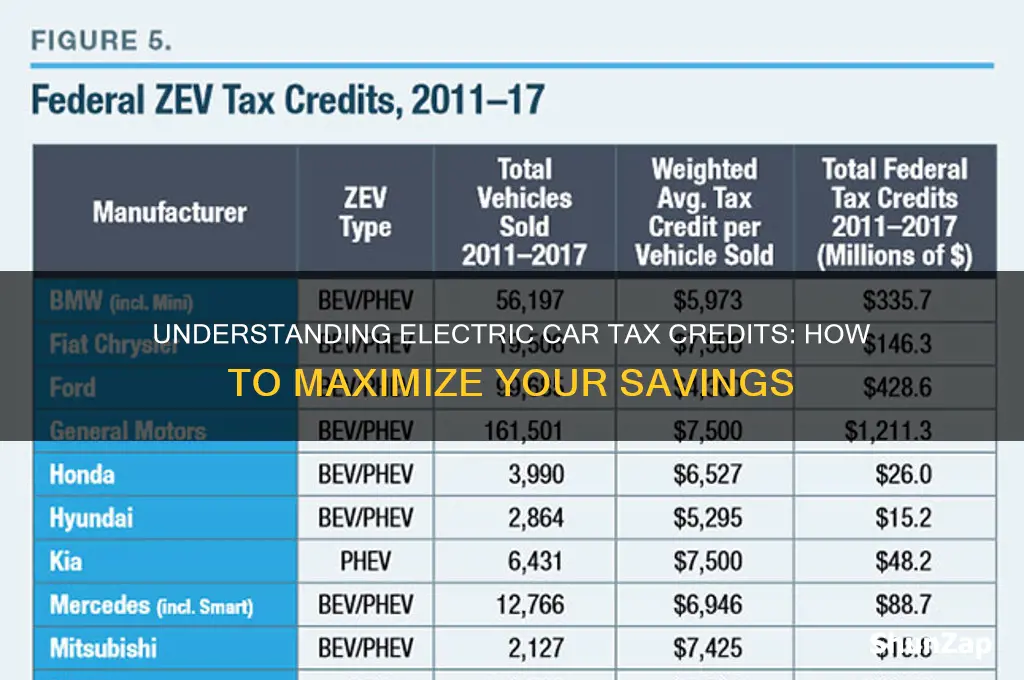

Manufacturer Restrictions: The tax credit also includes restrictions based on the manufacturer. Each automaker has a cap on the number of vehicles eligible for the credit. Once a manufacturer sells 200,000 qualifying vehicles, a phase-out period begins, during which the credit is gradually reduced. After this threshold, the credit is halved for the next two quarters, then reduced to 25% for the following two quarters, and finally eliminated. As of recent updates, several major manufacturers have already reached this cap, making their vehicles ineligible for the credit unless new legislation extends or modifies the program.

Additional Considerations: It's important to note that the vehicle must be purchased for personal use and not for resale. Leased vehicles may also qualify for a tax credit, but the credit goes to the leasing company, which may pass on some of the benefits to the lessee. Additionally, the vehicle must be primarily used in the United States, and the taxpayer must have a tax liability to claim the credit. If the credit exceeds the taxpayer's liability, the excess may be carried forward to future tax years, but it cannot be refunded.

Understanding these eligibility requirements is essential for maximizing the benefits of the electric vehicle tax credit. Prospective buyers should carefully review their financial situation, the vehicle's price, and the manufacturer's status to ensure they meet all criteria before making a purchase. Consulting with a tax professional can also provide valuable guidance tailored to individual circumstances.

Electric Guitar Strings: Types, Materials, and Choosing the Right Set

You may want to see also

Explore related products

![]()

Credit Amount: Maximum credit value, phase-out rules, and how it’s applied to taxes owed

The electric vehicle (EV) tax credit, officially known as the Qualified Plug-In Electric Drive Motor Vehicle Credit, is designed to incentivize the purchase of electric and hybrid vehicles. One of the most critical aspects of this credit is understanding the credit amount, including its maximum value, phase-out rules, and application to taxes owed. As of recent updates, the maximum credit value for eligible EVs is $7,500, but this amount is not universal and depends on specific criteria, such as the vehicle's battery capacity and the manufacturer's sales milestones. For instance, vehicles must have a battery capacity of at least 16 kilowatt-hours (kWh) to qualify for the full credit, with smaller batteries receiving a partial credit based on their capacity.

The phase-out rules are a crucial component of the EV tax credit. Once a manufacturer sells 200,000 qualifying vehicles in the U.S., the credit begins to phase out for that manufacturer's vehicles. The phase-out occurs in two stages: the credit is reduced by 50% for the next two quarters, then by 25% for the following two quarters, before being completely eliminated. As of 2023, manufacturers like Tesla and General Motors have already surpassed the 200,000-vehicle threshold, meaning their vehicles no longer qualify for the credit. Prospective buyers should verify a manufacturer's status before assuming eligibility for the tax credit.

The EV tax credit is a non-refundable credit, meaning it can reduce your tax liability to zero but does not provide a refund if the credit exceeds your tax owed. For example, if you owe $6,000 in taxes and qualify for the full $7,500 credit, your tax liability would be reduced to zero, but you would not receive the remaining $1,500 as a refund. However, the Inflation Reduction Act of 2022 introduced a provision allowing eligible lower-income buyers to transfer the credit to the dealership at the point of sale, effectively reducing the purchase price of the vehicle. This transferability is limited to specific income thresholds and vehicle price caps.

To apply the credit to taxes owed, you must file IRS Form 8936 with your federal tax return. The credit is claimed in the year the vehicle is placed into service, typically the year of purchase. It’s essential to retain documentation, such as the vehicle’s VIN and proof of purchase, to substantiate your claim. Additionally, the credit cannot be carried forward to future tax years, so it’s beneficial to plan your purchase and tax situation to maximize the credit’s value.

Lastly, the EV tax credit is subject to additional requirements under the Inflation Reduction Act, including assembly in North America and critical mineral/battery component sourcing rules. These rules are phased in over time, with increasing percentages of battery components and critical minerals required to be sourced from North America or countries with free trade agreements. Buyers should ensure their vehicle meets these criteria to qualify for the credit. Understanding these details ensures you can fully leverage the EV tax credit while complying with all eligibility requirements.

Are BMW Electric Cars Worth It? Pros, Cons, and Performance Review

You may want to see also

Explore related products

![]()

Qualifying Vehicles: Criteria for EVs, including battery size, assembly location, and model eligibility

To qualify for the electric vehicle (EV) tax credit, it’s essential to understand the specific criteria for eligible vehicles. The Qualifying Vehicles section focuses on three key areas: battery size, assembly location, and model eligibility. First, battery size plays a critical role. The vehicle must be equipped with a battery pack with a capacity of at least 7 kilowatt-hours (kWh) to qualify for the credit. This ensures the vehicle is a true EV or plug-in hybrid electric vehicle (PHEV) with substantial electric range, rather than a mild hybrid. The larger the battery capacity, the greater the potential credit, up to a maximum of $7,500, depending on other factors.

Second, the assembly location of the vehicle is a new requirement under recent legislation. To qualify, the EV must be assembled in North America, as defined by the United States, Canada, or Mexico. This criterion aims to incentivize domestic manufacturing and reduce reliance on foreign production. Buyers can verify a vehicle’s assembly location by checking the manufacturer’s label typically found on the driver’s side door jamb, which lists the country of origin.

Third, model eligibility is determined by the vehicle’s manufacturer suggested retail price (MSRP) and its classification as a car, truck, or SUV. For cars, the MSRP must not exceed $55,000, while trucks and SUVs must not exceed $80,000. Additionally, the vehicle must be new and used primarily for personal, not commercial, purposes. It’s important to note that certain high-income individuals and repeat claimants may face restrictions, and not all models from every manufacturer qualify, as some have surpassed the cap of 200,000 eligible vehicles sold.

Another critical aspect of model eligibility is the battery component requirement. A percentage of the battery’s critical minerals and components must be sourced from North America or countries with which the U.S. has a free trade agreement. This percentage increases annually, starting at 40% in 2023 and rising to 80% by 2027. Vehicles not meeting these thresholds may receive a reduced credit or none at all.

Lastly, buyers should consult the IRS’s list of eligible vehicles and the Department of Energy’s guidelines to ensure their chosen EV meets all criteria. Manufacturers are responsible for certifying their vehicles’ eligibility, and this information is typically available on their websites or through dealerships. By carefully reviewing these criteria—battery size, assembly location, and model eligibility—buyers can confidently determine whether their desired EV qualifies for the tax credit.

Electric Cars: Environmental Benefits, Cost Savings, and Future Potential Explored

You may want to see also

Explore related products

![]()

Claiming Process: How to file for the credit on tax returns and required documentation

To claim the electric car tax credit on your tax returns, you must follow a specific process and provide the necessary documentation. The first step is to ensure that the vehicle you purchased qualifies for the credit. This typically includes fully electric vehicles (EVs), plug-in hybrid electric vehicles (PHEVs), and fuel cell vehicles. The IRS provides a list of eligible vehicles, and the credit amount can vary depending on the vehicle's battery capacity and other factors. Once you confirm eligibility, you can proceed with the claiming process.

The primary form used to claim the electric vehicle tax credit is IRS Form 8936, titled "Qualified Plug-in Electric Drive Motor Vehicle Credit." This form requires detailed information about the vehicle, including the make, model, and Vehicle Identification Number (VIN). You must also provide the date the vehicle was placed in service, which is generally the date of purchase. Additionally, Form 8936 will ask for the credit amount you are claiming, which is calculated based on the vehicle's battery capacity, up to a maximum credit limit set by law.

When filing your tax return, attach Form 8936 to your Form 1040 or Form 1040-SR. Ensure that all sections of Form 8936 are completed accurately to avoid delays or rejections. It’s crucial to report the correct credit amount, as overclaiming can result in audits or penalties. If you are using tax preparation software, it will typically guide you through the process and ensure the form is correctly integrated into your return. However, double-checking the information is always a good practice.

Required documentation includes the vehicle’s purchase agreement or sales contract, which verifies the purchase price and date. You may also need the manufacturer’s certification that the vehicle qualifies for the credit, often provided at the time of purchase. Keep these documents readily available, as the IRS may request them in case of an audit. Additionally, if the vehicle is leased, the leasing company may claim the credit, and you should confirm this with them to avoid duplicate claims.

Finally, be aware of any phase-out rules that may apply to the electric vehicle tax credit. For some manufacturers, the credit begins to phase out once they sell a certain number of qualifying vehicles. The IRS provides updates on which manufacturers have reached the phase-out threshold, so check their website for the latest information. By carefully following these steps and maintaining proper documentation, you can successfully claim the electric car tax credit on your tax returns.

Illinois Communities Powered by Ameren Electric: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Recent Changes: Updates to tax credit laws, including Inflation Reduction Act modifications

The electric vehicle (EV) tax credit landscape has undergone significant transformations in recent years, with the Inflation Reduction Act (IRA) of 2022 being a pivotal piece of legislation. This act introduced substantial modifications to the existing tax credit structure, aiming to accelerate the adoption of electric vehicles and reduce greenhouse gas emissions. One of the most notable changes is the extension of the tax credit program, which was initially set to expire after a certain number of vehicles sold per manufacturer. The IRA removes this manufacturer-specific cap, allowing all eligible EVs to qualify for the credit, regardless of the producer's sales volume. This shift ensures a more level playing field for both established automakers and new entrants in the EV market.

Under the new regulations, the tax credit amount remains at a maximum of $7,500 but is now divided into two parts, each with specific requirements. The first $3,750 is contingent on the vehicle's battery capacity and the sourcing of critical minerals. To qualify, a certain percentage of the battery's critical minerals must be extracted or processed in the United States or a country with which it has a free trade agreement. This provision aims to reduce reliance on foreign supply chains and encourage domestic production. The remaining $3,750 is tied to battery component manufacturing or assembly in North America, further emphasizing the IRA's focus on localizing the EV supply chain.

Another crucial update is the introduction of income and vehicle price caps. The tax credit is now available only to individuals with modified adjusted gross incomes below specified thresholds, ensuring that the benefit targets middle- and lower-income buyers. Additionally, the credit applies solely to vehicles with manufacturer suggested retail prices (MSRP) below certain limits, which vary by vehicle type (e.g., cars, trucks, SUVs). These caps prevent the credit from being utilized for luxury vehicles and ensure that the incentive supports more affordable EV options.

The IRA also mandates that eligible vehicles must undergo final assembly in North America, marking a significant shift towards promoting regional manufacturing. This requirement, effective immediately, means that EVs assembled outside this region no longer qualify for the tax credit. Such a change has prompted automakers to reconsider their production strategies, potentially leading to increased investment in North American manufacturing facilities.

Furthermore, the Act introduces a new provision for used electric vehicles, offering a tax credit of up to $4,000 or 30% of the vehicle's price, whichever is less. This credit is available for used EVs that are at least two years old and meet specific price and income requirements. By extending incentives to the pre-owned market, the IRA aims to make electric vehicles more accessible to a broader range of consumers, thereby accelerating the transition to a more sustainable transportation sector. These recent changes collectively represent a comprehensive overhaul of the EV tax credit system, aligning it with broader environmental and economic goals.

Powering the Grid: Exploring the Gas Behind Electricity Generation

You may want to see also

Frequently asked questions

The electric car tax credit is a federal incentive designed to encourage the purchase of electric vehicles (EVs). It allows eligible buyers to claim a tax credit of up to $7,500 on their federal income taxes, reducing the overall cost of the vehicle. The credit amount depends on the battery capacity and other criteria set by the IRS.

Eligibility for the electric car tax credit depends on factors like the vehicle’s battery size, manufacturer’s sales volume, and the buyer’s tax liability. The credit phases out once a manufacturer sells 200,000 qualifying vehicles. Additionally, the buyer must have sufficient tax liability to claim the full credit.

Yes, the federal electric car tax credit can often be combined with state and local incentives, such as rebates, tax credits, or reduced registration fees. However, the availability and amount of these incentives vary by state, so it’s important to check local programs for additional savings.