The 7500 electric car tax credit is a federal incentive designed to promote the adoption of electric vehicles (EVs) in the United States. This credit, officially known as the Qualified Plug-in Electric Drive Motor Vehicle Tax Credit, allows eligible taxpayers to claim up to $7,500 on their federal income tax return when purchasing a new electric or plug-in hybrid vehicle. The credit amount varies depending on the vehicle's battery capacity, with larger batteries qualifying for the full credit. To be eligible, the vehicle must meet specific requirements, such as being new, purchased for personal use, and manufactured by a qualified automaker. Additionally, the credit phases out for each manufacturer once they sell 200,000 qualifying vehicles, making it essential for buyers to verify eligibility before purchase. Understanding how this tax credit works can significantly reduce the upfront cost of an electric vehicle, making it a more accessible and appealing option for environmentally conscious consumers.

Explore related products

What You'll Learn

- Eligibility Requirements: Income limits, vehicle price caps, and battery sourcing rules for qualification

- New vs. Used Cars: Different credit amounts and criteria for new and used electric vehicles

- Credit Application Process: How to claim the credit on federal tax returns

- Manufacturer Caps: Limitations on credits per automaker based on sales thresholds

- Phaseout Schedule: Timeline for credit reduction and eventual expiration based on industry milestones

![]()

Eligibility Requirements: Income limits, vehicle price caps, and battery sourcing rules for qualification

The $7,500 electric vehicle (EV) tax credit, officially known as the Qualified Plug-In Electric Drive Motor Vehicle Credit, is a federal incentive designed to promote the adoption of electric vehicles. However, not all EVs or buyers qualify for this credit. Eligibility is determined by specific criteria, including income limits, vehicle price caps, and battery sourcing rules. Understanding these requirements is crucial for anyone considering purchasing an EV to maximize their potential tax savings.

Income Limits play a significant role in determining eligibility for the $7,500 tax credit. As of the latest updates, the credit begins to phase out for single filers with a modified adjusted gross income (MAGI) above $150,000, head of household filers above $225,000, and joint filers above $300,000. Once a taxpayer’s income exceeds these thresholds, the credit is reduced incrementally until it is completely phased out. For example, if a single filer’s MAGI is $160,000, they would not qualify for the full $7,500 credit. This income-based limitation ensures that the tax credit benefits middle- and lower-income buyers rather than higher-income individuals.

Vehicle Price Caps are another critical eligibility requirement. To qualify for the tax credit, the manufacturer’s suggested retail price (MSRP) of the EV must be below a certain threshold. For vans, SUVs, and pickup trucks, the cap is set at $80,000, while for other vehicle types, it is $55,000. Vehicles exceeding these price limits are ineligible for the credit. This rule prevents luxury EVs from qualifying, aligning the incentive with the goal of making electric mobility more accessible to a broader audience.

Battery Sourcing Rules have been introduced to encourage domestic production and reduce reliance on foreign materials. To qualify for the full $7,500 credit, a certain percentage of the EV’s battery components must be manufactured or assembled in North America. Additionally, a portion of the critical minerals used in the battery must be extracted or processed in the United States or a country with which it has a free trade agreement. These requirements are phased in over time, with increasing thresholds each year. Failure to meet these battery sourcing criteria can result in a reduced or eliminated credit, emphasizing the importance of verifying a vehicle’s compliance before purchase.

In summary, eligibility for the $7,500 electric car tax credit hinges on meeting specific income limits, adhering to vehicle price caps, and satisfying battery sourcing rules. Prospective EV buyers should carefully review these requirements to ensure they qualify for the full credit. By doing so, they can take full advantage of this federal incentive, making the transition to electric vehicles more affordable and environmentally beneficial.

The Brain of Electric Vehicles: Understanding the ECU

You may want to see also

Explore related products

![]()

New vs. Used Cars: Different credit amounts and criteria for new and used electric vehicles

The $7,500 federal tax credit for electric vehicles (EVs) is a significant incentive for buyers, but it’s important to understand that the credit amounts and eligibility criteria differ between new and used electric cars. For new EVs, the full $7,500 credit is available, but it’s not automatic. The vehicle must meet specific requirements, such as being manufactured by a qualified automaker and having a battery capacity of at least 16 kilowatt-hours. Additionally, the credit phases out once an automaker sells 200,000 qualifying vehicles, affecting brands like Tesla and General Motors. Buyers must also meet income limits and ensure the car is for personal use, not resale. This credit directly reduces the federal taxes owed, but it’s non-refundable, meaning it can’t result in a tax refund if the credit exceeds the tax liability.

For used EVs, the rules are different under the Inflation Reduction Act. Buyers of qualified used electric vehicles can receive a tax credit of up to $4,000, or 30% of the vehicle’s sale price, whichever is less. To qualify, the car must be at least two years old, cost $25,000 or less, and be purchased from a licensed dealer. Income limits also apply, with individuals capped at $75,000 and joint filers at $150,000. Unlike the new car credit, the used EV credit is refundable, meaning buyers can receive the full amount even if they have no tax liability. This makes it particularly beneficial for lower-income individuals looking to transition to electric vehicles.

The criteria for eligibility also vary between new and used EVs. For new cars, the vehicle must be purchased new and never previously owned, while used cars must meet age and price requirements. Both categories require the buyer to be the original purchaser for tax credit purposes. Additionally, the vehicle’s battery and assembly must meet specific domestic content requirements under the new rules, which are phased in over time. These requirements are more stringent for new EVs, while used EVs are exempt from these sourcing rules.

Another key difference is the application process. For new EVs, the credit is claimed on your federal tax return using IRS Form 8936. Starting in 2024, buyers can transfer the credit to the dealership at the point of sale, effectively reducing the purchase price. For used EVs, the credit is claimed using Form 8936 as well, but the refundable nature simplifies the process for those with limited tax liability. It’s crucial to retain documentation, such as the vehicle’s VIN and purchase price, to substantiate the claim.

In summary, while both new and used electric vehicles qualify for tax credits, the amounts, eligibility criteria, and application processes differ significantly. New EVs offer a higher credit of up to $7,500 but come with stricter manufacturer and buyer requirements. Used EVs provide a smaller but still valuable credit of up to $4,000, with more flexibility in terms of vehicle age and price. Understanding these distinctions can help buyers maximize their savings and make informed decisions when purchasing an electric vehicle.

Norway's Electrical Plug Type: A Comprehensive Guide for Travelers

You may want to see also

Explore related products

![]()

Credit Application Process: How to claim the credit on federal tax returns

The $7,500 electric vehicle (EV) tax credit, formally known as the Qualified Plug-In Electric Drive Motor Vehicle Credit, is a federal incentive designed to promote the adoption of electric vehicles. To claim this credit on your federal tax returns, you must follow a specific application process outlined by the Internal Revenue Service (IRS). The first step is to ensure your vehicle qualifies for the credit. It must be a new, recently purchased or leased plug-in electric vehicle with a battery capacity of at least 5 kilowatt-hours. Additionally, the vehicle must be acquired for personal use, not for resale, and it must be placed in service during the tax year for which you are claiming the credit.

Once you confirm eligibility, the next step is to complete the necessary IRS forms when filing your federal tax return. The primary form for claiming the EV tax credit is Form 8936, Qualified Plug-In Electric Drive Motor Vehicle Credit. This form requires details about the vehicle, including its make, model, and Vehicle Identification Number (VIN), as well as the date it was placed in service. You must also provide information about the battery capacity, as the credit amount is partially determined by this factor. The credit ranges from $2,500 to $7,500, depending on the battery size, with an additional $417 for each kilowatt-hour of battery capacity over 5 kilowatt-hours, up to a maximum of $7,500.

After completing Form 8936, you will transfer the calculated credit amount to your Form 1040, U.S. Individual Income Tax Return, specifically on Schedule 3 (Additional Credits and Payments). This ensures the credit is applied directly to your tax liability. It’s important to note that the credit is non-refundable, meaning it can reduce your tax liability to zero but cannot result in a refund if the credit exceeds your tax owed. However, any unused portion of the credit can be carried forward to future tax years, provided the vehicle remains eligible.

To avoid delays or rejections, ensure all information on Form 8936 is accurate and matches the details provided by the vehicle manufacturer or dealer. The IRS may require additional documentation, such as the vehicle’s sales contract or lease agreement, to verify eligibility. It’s also advisable to retain all records related to the purchase or lease of the EV, as well as the tax forms submitted, for at least three years in case of an audit.

Finally, consider consulting a tax professional or using tax preparation software to navigate the application process, especially if you have a complex financial situation. These resources can help ensure you maximize the credit and comply with all IRS requirements. By following these steps and providing the necessary documentation, you can successfully claim the $7,500 electric vehicle tax credit on your federal tax returns.

Electric Vehicle Tax Credit: Is It Refundable?

You may want to see also

Explore related products

![]()

Manufacturer Caps: Limitations on credits per automaker based on sales thresholds

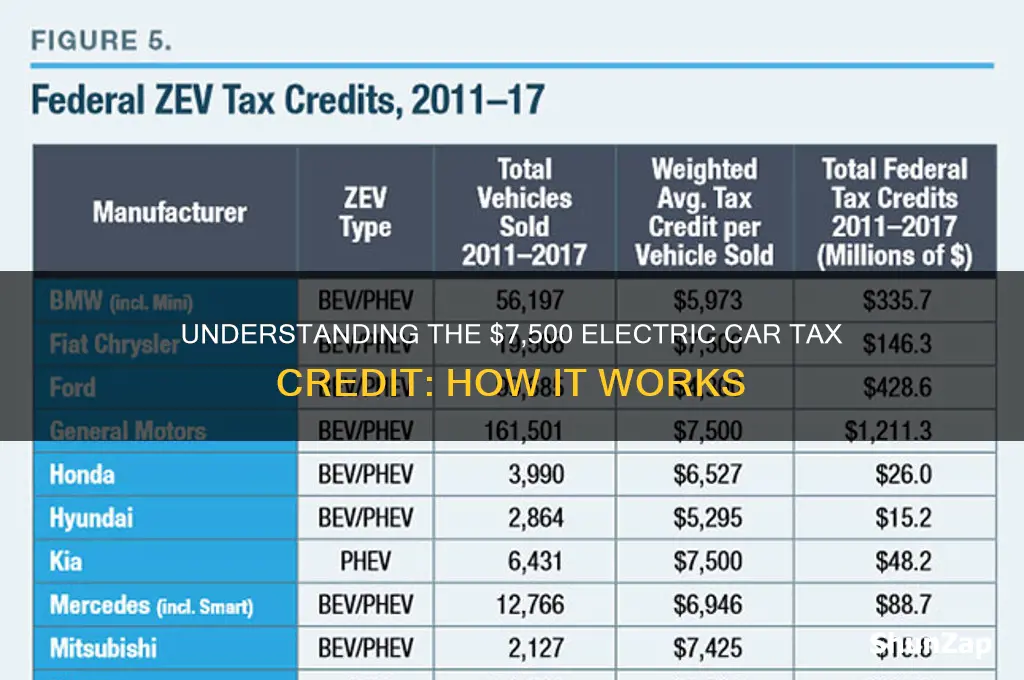

The $7,500 electric vehicle (EV) tax credit, officially known as the Qualified Plug-in Electric Drive Motor Vehicle Credit, includes a critical component called Manufacturer Caps, which impose limitations on the number of credits available per automaker based on their cumulative EV sales. These caps are designed to phase out the tax credit for manufacturers once they reach specific sales thresholds, ensuring the incentive remains targeted and fiscally sustainable. Under the current rules, once an automaker sells 200,000 qualifying EVs in the U.S., a phasedown of the tax credit begins. This means that for the subsequent two quarters, the credit is reduced to 50% of its original value ($3,750), and for the following two quarters, it drops to 25% ($1,875), before being eliminated entirely.

The Manufacturer Caps are applied on a per-manufacturer basis, not per model or brand. For example, if a company like Tesla or General Motors reaches the 200,000-unit threshold, all of their qualifying EV models become ineligible for the full credit once the phaseout begins. This system incentivizes early adoption of EVs while preventing the tax credit from becoming an open-ended subsidy for high-volume manufacturers. It also encourages automakers to innovate and reduce costs to remain competitive once the credits expire.

To track sales and enforce the caps, the IRS maintains a public tally of qualifying EV sales reported by manufacturers. Prospective buyers can check this list to determine if a specific automaker has triggered the phaseout process. For instance, Tesla and General Motors have already surpassed the 200,000-unit threshold, making their vehicles ineligible for the credit, while other manufacturers like Ford or Volkswagen may still have credits available, depending on their cumulative sales.

The Manufacturer Caps also highlight the importance of timing for consumers. Buyers interested in purchasing an EV from a manufacturer nearing the sales threshold should act quickly to secure the full $7,500 credit before the phaseout begins. Additionally, these caps underscore the need for automakers to plan strategically, as the loss of the tax credit can impact consumer demand for their EV models.

In summary, Manufacturer Caps are a key feature of the $7,500 electric car tax credit, limiting the availability of credits based on an automaker’s cumulative EV sales. This mechanism ensures the incentive remains effective and equitable, while also encouraging early market growth and long-term sustainability in the EV industry. Buyers and manufacturers alike must stay informed about sales thresholds and phaseout timelines to maximize the benefits of this program.

Electric Vehicles: Worth the Cost?

You may want to see also

Explore related products

![]()

Phaseout Schedule: Timeline for credit reduction and eventual expiration based on industry milestones

The $7,500 electric vehicle (EV) tax credit, officially known as the Qualified Plug-In Electric Drive Motor Vehicle Credit, is subject to a phaseout schedule that reduces and eventually eliminates the credit based on industry milestones. This schedule is designed to gradually taper off the incentive as the EV market matures and achieves certain sales thresholds. The phaseout begins once an automaker sells 200,000 qualifying electric vehicles in the United States. At this point, a two-quarter phaseout period is triggered, during which the credit is reduced before expiring entirely.

The phaseout timeline is divided into two stages. In the first stage, which starts in the second quarter after the 200,000-unit threshold is reached, the credit is reduced to $3,750 for the subsequent two quarters. This reduction marks the beginning of the transition away from the full $7,500 credit. In the second stage, the credit is further reduced to $1,875 for the following two quarters before expiring completely. This structured reduction ensures a gradual transition, allowing consumers and manufacturers to adjust to the changing incentive landscape.

It’s important to note that the phaseout applies on a per-manufacturer basis, meaning each automaker has its own independent timeline based on its cumulative EV sales. For example, Tesla and General Motors have already reached the 200,000-unit threshold and completed their phaseout periods, rendering their vehicles ineligible for the credit. Other manufacturers, such as Ford and Toyota, are still offering the full credit for eligible models as they have not yet hit the sales milestone.

The phaseout schedule reflects the government’s intention to use the tax credit as a temporary tool to stimulate the EV market rather than a permanent subsidy. As the industry grows and economies of scale reduce production costs, the need for incentives diminishes. The timeline is tied to industry milestones, ensuring that the credit phases out as EVs become more mainstream and competitive with traditional internal combustion engine vehicles.

For consumers, understanding the phaseout schedule is crucial for maximizing the tax credit’s benefits. Prospective EV buyers should research whether their preferred manufacturer has reached the 200,000-unit threshold and is in the phaseout period. Additionally, staying informed about updates to the credit, such as those introduced by the Inflation Reduction Act of 2022, can help buyers navigate eligibility requirements and plan their purchases accordingly. As the EV market continues to evolve, the phaseout schedule will remain a key factor in the availability and value of the $7,500 tax credit.

Materials for Electrical Switches: Understanding Key Components and Their Uses

You may want to see also

Frequently asked questions

The 7500 electric car tax credit is a federal incentive in the U.S. that allows taxpayers to claim up to $7,500 as a tax credit when purchasing a qualifying new electric vehicle (EV). Eligibility depends on the vehicle meeting specific criteria, such as battery capacity and manufacturer production limits, and the taxpayer’s tax liability.

The $7,500 tax credit directly reduces the amount of federal income tax you owe. It is non-refundable, meaning it can only lower your tax liability to zero but won’t provide a refund if the credit exceeds your tax owed. You claim the credit when filing your federal tax return using IRS Form 8936.

Yes, the Inflation Reduction Act of 2022 introduced new restrictions, including income limits, vehicle price caps, and requirements for North American assembly. Additionally, the credit is phased out once a manufacturer sells 200,000 qualifying vehicles, and it now applies to both new and used EVs, with a reduced credit amount for used vehicles.