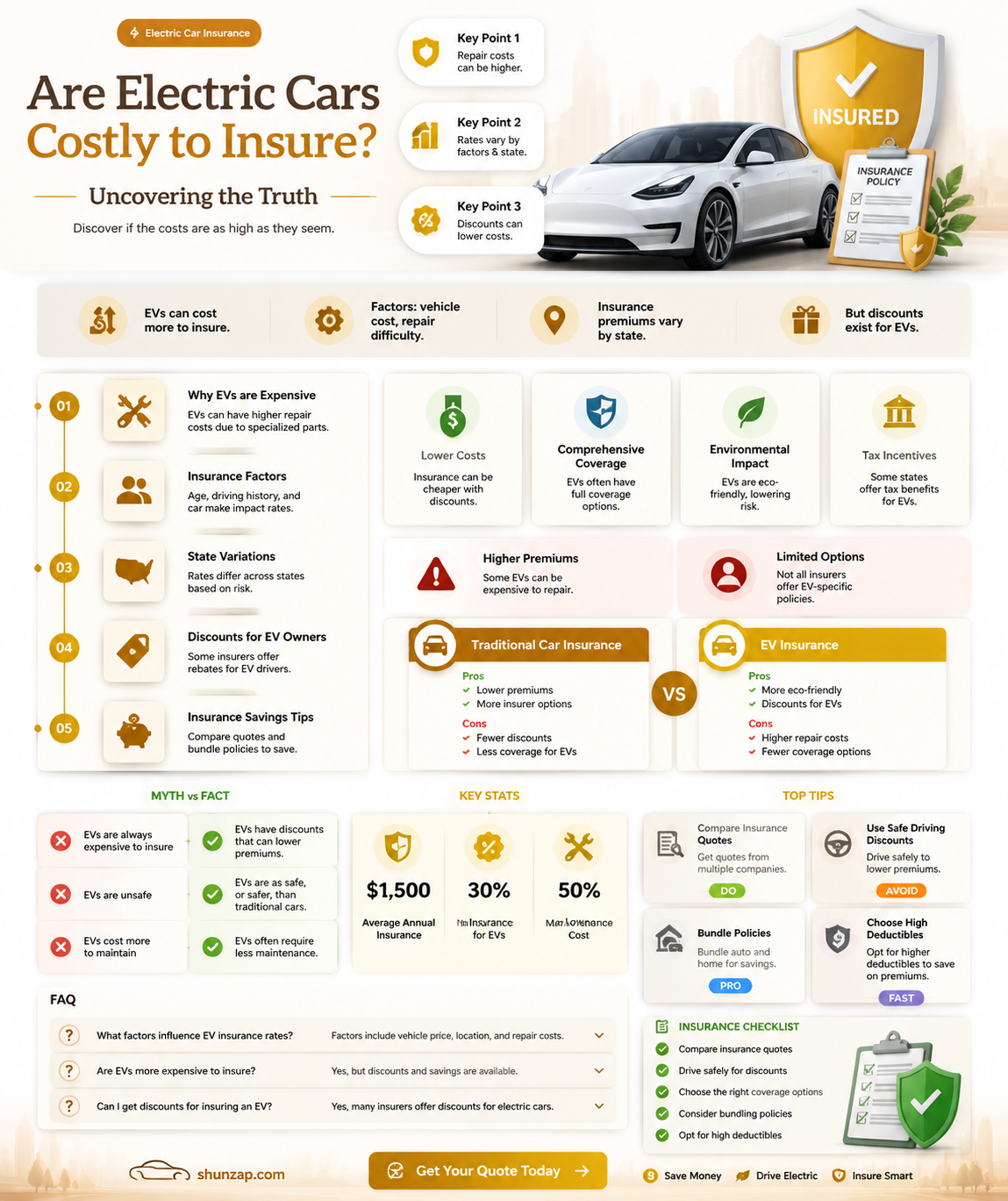

When considering the cost of insuring electric cars, many potential buyers wonder whether these vehicles are inherently more expensive to insure compared to traditional gasoline-powered cars. The answer is not straightforward, as insurance premiums for electric cars depend on various factors, including the make and model of the vehicle, the driver's history, and the insurance company's policies. Generally, electric cars may have higher upfront costs due to advanced technology and battery systems, which can lead to higher repair or replacement expenses in the event of an accident. However, some insurance companies offer discounts for eco-friendly vehicles, potentially offsetting these costs. Additionally, factors like lower maintenance requirements and government incentives might influence overall insurance rates. Ultimately, while electric cars can be more expensive to insure in some cases, it's essential to compare quotes and consider individual circumstances to determine the actual cost.

| Characteristics | Values |

|---|---|

| General Insurance Cost | Electric cars are often more expensive to insure than traditional gas-powered vehicles. |

| Reasons for Higher Costs | Higher repair costs due to specialized parts and technology. |

| Limited availability of repair shops and trained technicians. | |

| Higher vehicle purchase price, leading to higher replacement costs. | |

| Exceptions | Some electric vehicles (e.g., Tesla Model 3) may have lower insurance rates due to advanced safety features. |

| Insurance Discounts | Discounts may be available for safety features like autonomous driving and collision avoidance systems. |

| Regional Variations | Insurance costs vary by location due to local regulations, theft rates, and repair costs. |

| Battery Replacement Costs | High costs associated with replacing electric vehicle batteries can impact insurance premiums. |

| Theft Rates | Lower theft rates for some electric vehicles may offset higher repair costs in certain cases. |

| Maintenance Costs | Lower maintenance costs for electric vehicles may reduce overall insurance expenses over time. |

| Insurance Company Policies | Some insurers offer specialized policies for electric vehicles, which may include unique coverage options. |

| Government Incentives | Government incentives for electric vehicles may indirectly affect insurance costs by increasing adoption rates. |

| Future Trends | As electric vehicle technology becomes more widespread, insurance costs are expected to decrease. |

Explore related products

$19.99 $19.99

What You'll Learn

![]()

Insurance Costs by EV Model

When considering the insurance costs for electric vehicles (EVs), it’s important to recognize that premiums can vary significantly depending on the specific model. Factors such as the car’s value, repair costs, safety features, and theft rates play a crucial role in determining insurance rates. For instance, high-end EVs like the Tesla Model S or Porsche Taycan tend to have higher insurance costs due to their expensive parts and advanced technology, which can be costly to repair or replace. On the other hand, more affordable models like the Nissan Leaf or Chevrolet Bolt EV often come with lower insurance premiums because their repair costs are generally less prohibitive.

Mid-range EVs, such as the Tesla Model 3 or Hyundai Kona Electric, fall somewhere in between. While they may still have higher insurance costs compared to their gasoline counterparts, they are often more affordable to insure than luxury EVs. The Model 3, for example, benefits from Tesla’s advanced safety features, which can sometimes offset higher repair costs by reducing the likelihood of accidents. Similarly, the Hyundai Kona Electric’s competitive pricing and widespread availability of parts can make it a more cost-effective option for insurance.

Compact and entry-level EVs, like the Mini Cooper SE or Fiat 500e, typically have lower insurance costs due to their smaller size, lower price tags, and simpler technology. These vehicles are less expensive to repair and often have fewer high-tech components that could drive up insurance premiums. However, it’s worth noting that even within this category, insurance costs can vary based on the specific model and its safety ratings.

Luxury EVs, such as the Audi e-tron or Mercedes-Benz EQS, are among the most expensive to insure due to their high purchase prices and sophisticated systems. These vehicles often feature cutting-edge technology and premium materials, which can significantly increase repair costs. Additionally, their higher theft rates and greater potential for damage in accidents contribute to elevated insurance premiums. Prospective buyers of luxury EVs should be prepared for higher insurance costs as part of their overall ownership expenses.

Lastly, it’s essential to consider how insurance companies assess risk for EVs. Some insurers offer discounts for EVs due to their environmental benefits or safety features, while others may charge more due to the perceived risks associated with new technology. Shopping around and comparing quotes from multiple insurers can help EV owners find the best rates for their specific model. Ultimately, while not all electric cars are expensive to insure, the costs can vary widely based on the make, model, and other factors unique to each vehicle.

Electric Vehicles: Environmental Friend or Foe?

You may want to see also

Explore related products

![]()

Factors Affecting EV Insurance Rates

Electric vehicle (EV) insurance rates are influenced by a variety of factors, making it essential for potential EV owners to understand what drives these costs. One of the primary factors is the vehicle’s value and repair costs. Electric cars often come with higher price tags due to advanced technology, such as battery systems and electric motors. Additionally, repairs can be more expensive because specialized parts and trained technicians are required. Insurers factor these costs into premiums, which can result in higher insurance rates for EVs compared to traditional gasoline vehicles.

Another significant factor affecting EV insurance rates is the risk of theft or damage. Some electric vehicles, particularly high-end models, are targets for theft due to their resale value and desirability. Moreover, the cost of replacing or repairing expensive components like batteries can significantly impact insurance claims. Insurers may charge higher premiums for EVs perceived to be at greater risk of theft or damage. However, features like advanced security systems and GPS tracking in many EVs can sometimes mitigate these risks and lower insurance costs.

The driver’s location and usage patterns also play a crucial role in determining EV insurance rates. Urban areas with higher traffic density and crime rates generally lead to more accidents and thefts, resulting in elevated premiums. Additionally, how the EV is used—whether for daily commuting, long-distance travel, or occasional driving—affects risk assessment. Insurers may offer lower rates for drivers who use their EVs less frequently or in safer environments.

Driver history and demographics are universal factors in insurance pricing, and they apply to EVs as well. Drivers with a clean record and no history of accidents or claims typically enjoy lower premiums. Conversely, younger or inexperienced drivers, as well as those with a history of violations, may face higher costs. Insurers also consider factors like age, gender, and credit score, as these are statistically linked to risk levels.

Lastly, available discounts and incentives can offset some of the higher costs associated with EV insurance. Many insurers offer discounts for safety features common in EVs, such as automatic emergency braking, lane-keeping assist, and anti-theft systems. Additionally, some states or insurance companies provide incentives for owning eco-friendly vehicles, which can reduce premiums. Shopping around and comparing policies can help EV owners find the most cost-effective coverage tailored to their needs.

In summary, while not all electric cars are expensive to insure, factors like vehicle value, repair costs, theft risk, location, driver history, and available discounts significantly influence EV insurance rates. Understanding these factors allows potential EV owners to make informed decisions and potentially lower their insurance expenses.

Understanding Electric Vehicle Performance Through kWh Ratings

You may want to see also

Explore related products

![]()

Comparing EV vs. Gas Car Premiums

When comparing insurance premiums for electric vehicles (EVs) versus traditional gas-powered cars, several factors come into play. Generally, EVs tend to have higher insurance premiums than their gas counterparts. This is primarily due to the higher cost of repairs and replacement parts for electric vehicles. EVs are equipped with advanced technology, such as lithium-ion batteries and electric motors, which are more expensive to fix or replace after an accident. Additionally, the specialized labor required to service EVs often comes at a premium, further driving up insurance costs.

Another factor influencing insurance premiums is the initial purchase price of the vehicle. EVs, especially newer models, often have a higher sticker price compared to gas cars in the same class. Since insurance premiums are partly based on the vehicle's value, higher-priced EVs typically result in more expensive policies. However, it’s important to note that this isn’t universal; some affordable EVs may have premiums closer to those of gas cars, depending on the model and insurer.

Driving habits and risk profiles also play a role in insurance costs. EVs are often marketed toward environmentally conscious drivers, who may be perceived as safer on the road. However, the data on this is mixed, and insurers still consider factors like mileage, location, and driver history. Interestingly, some insurers offer discounts for EV owners as part of green initiatives, which can offset the higher base premium. These discounts vary by provider and region, so it’s worth shopping around for EV-specific policies.

When comparing premiums directly, gas cars often benefit from decades of established repair networks and lower parts costs, making them cheaper to insure. For example, a mid-range gas sedan might have an annual premium of $1,200, while a comparable EV could cost $1,500 or more. However, this gap is narrowing as EVs become more common and repair infrastructure expands. Additionally, maintenance savings for EVs—due to fewer moving parts and no need for oil changes—can partially offset higher insurance costs over time.

Finally, geographic location significantly impacts insurance premiums for both EVs and gas cars. In areas with robust EV infrastructure and higher adoption rates, insurers may offer more competitive rates for electric vehicles. Conversely, in regions with limited charging stations or higher theft rates for EVs, premiums can be even steeper. To make an informed decision, drivers should obtain quotes for both types of vehicles and consider their long-term ownership costs, including insurance, maintenance, and fuel savings. While EVs may have higher premiums, their total cost of ownership can still be competitive when all factors are considered.

Electric Vehicles in Brookhaven: Exploring the Options

You may want to see also

Explore related products

$23.99

![]()

Impact of Repair Costs on Insurance

The cost of repairing electric vehicles (EVs) plays a significant role in determining their insurance premiums. Electric cars often feature advanced technology, including high-voltage batteries, electric motors, and sophisticated electronics. When these components are damaged, repairs can be more complex and costly compared to traditional internal combustion engine (ICE) vehicles. For instance, replacing a battery pack in an EV can cost several thousand dollars, whereas a conventional car’s engine repair might be less expensive. Insurers factor these higher repair costs into their risk assessments, often resulting in higher premiums for electric vehicles.

Another factor contributing to the impact of repair costs on insurance is the limited availability of specialized repair facilities and technicians. Not all auto repair shops are equipped to handle electric vehicles, and those that are often charge a premium for their services. This scarcity drives up labor costs, which insurers must account for when calculating premiums. Additionally, the time required to repair EVs can be longer due to the complexity of the systems involved, further increasing costs. As a result, insurers may view EVs as riskier to insure, leading to higher rates for policyholders.

The use of lightweight and exotic materials in electric vehicles also influences repair costs. Many EVs incorporate materials like carbon fiber and aluminum to reduce weight and improve efficiency. While these materials enhance performance, they are often more expensive to repair or replace than traditional steel components. Even minor accidents can result in significant damage to these materials, leading to higher claims payouts for insurers. This, in turn, contributes to elevated insurance premiums for electric car owners.

Furthermore, the integration of advanced driver-assistance systems (ADAS) in many electric vehicles adds another layer of complexity to repairs. Features like adaptive cruise control, lane-keeping assist, and automatic emergency braking rely on sensors and cameras that are costly to replace or recalibrate after an accident. Insurers must consider the expense of repairing or replacing these systems when underwriting policies for EVs. The cumulative effect of these factors often results in higher insurance costs for electric vehicles compared to their ICE counterparts.

Lastly, the resale value and total loss thresholds of electric vehicles can impact insurance rates. If an EV is deemed a total loss after an accident, insurers must pay out the vehicle’s market value. However, the depreciation of EVs, particularly due to concerns about battery life, can complicate these calculations. Insurers may adjust premiums to account for the potential financial exposure associated with total loss claims. Thus, while not directly a repair cost, the interplay between vehicle value and repair expenses contributes to the overall insurance cost for electric cars.

In summary, the impact of repair costs on insurance for electric vehicles is multifaceted. The high cost of replacing advanced components, limited repair infrastructure, expensive materials, and integrated technology all contribute to higher insurance premiums. As the electric vehicle market evolves, insurers will continue to refine their models to accurately reflect these costs, but for now, many EVs remain more expensive to insure than traditional cars.

Ford's Electric Vehicle Future: Discontinuation Decision Explored

You may want to see also

Explore related products

![]()

Discounts for Electric Vehicle Owners

While the initial cost of electric vehicles (EVs) can be higher than their gasoline counterparts, insurance costs don't necessarily follow the same trend. In fact, many insurance companies offer discounts specifically for electric vehicle owners, making EV ownership more affordable than you might think.

Let's delve into the various discounts available and how they can benefit you.

Green Vehicle Discounts: Many insurers recognize the environmental benefits of EVs and incentivize their adoption. These discounts, often labeled as "green vehicle" or "eco-friendly" discounts, can range from 5% to 10% off your premium. Some companies even offer higher discounts for fully electric vehicles compared to hybrids.

Low Mileage Discounts: EVs are often driven less than traditional cars due to factors like shorter commutes and the availability of charging stations. This lower mileage translates to a reduced risk of accidents, and many insurers reward this with low mileage discounts. If you're a light driver, this discount can significantly lower your insurance costs.

Safety Feature Discounts: EVs are packed with advanced safety features like automatic emergency braking, lane departure warning, and adaptive cruise control. These features significantly reduce the likelihood of accidents, leading to lower insurance premiums. Insurers often offer discounts for vehicles equipped with these safety technologies, regardless of whether they're electric or not.

Home Charging Discounts: Some insurance companies offer discounts to EV owners who charge their vehicles at home. This is because home charging is generally considered safer and more controlled than public charging stations. Additionally, some insurers partner with charging network providers to offer further discounts or rewards for using their network.

State and Local Incentives: Beyond insurance company discounts, many states and local governments offer incentives for EV ownership, including potential reductions in registration fees and taxes. These incentives can further offset the cost of insuring your electric vehicle.

Remember, the availability and amount of discounts vary depending on your location, insurance provider, and specific EV model. It's crucial to shop around and compare quotes from multiple insurers to find the best deal for your electric vehicle. By taking advantage of these discounts, you can make owning an electric car a more financially viable and environmentally friendly choice.

Electric Vehicle Mileage Tax: Who Should Pay and Why?

You may want to see also

Frequently asked questions

Not necessarily. While some electric cars (EVs) may have higher insurance premiums due to their advanced technology and higher repair costs, others are comparable or even cheaper to insure than gasoline vehicles. Factors like safety ratings, theft rates, and driver history also play a significant role.

Electric cars can be more expensive to insure due to their higher purchase price, specialized parts, and the cost of repairing or replacing battery systems. Additionally, limited repair facilities and technicians for EVs can drive up labor costs, which insurers may factor into premiums.

Yes, many insurers offer competitive rates for electric cars, especially if the vehicle has high safety ratings, low theft rates, or qualifies for EV-specific discounts. Shopping around and comparing quotes can help you find affordable coverage tailored to your needs.